Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Maximizing Your Purchasing Potential

When it comes to purchasing a home, understanding your buying power and strategically taking steps to enhance your position are key to maximizing your purchasing potential. Beyond just envisioning your dream home, it is crucial to recognize the numerical factors lenders consider when approving you for a mortgage. By strengthening the following key areas, you can elevate your financial standing and position and find success in a competitive housing market.

Strategies to Maximize Your Purchasing Potential

First and foremost, give yourself time to prepare. Change will not happen overnight. Be patient and give yourself grace. Create a list of attainable goals and make consistent efforts to reach them. Over time, you will see the difference. We suggest talking to a lender as soon as possible so they can help identify specific key areas unique to you. Overall, you can increase your buying power by preparing for a down payment, increasing your credit score, and reducing your debit-to-income ratio.

Prepare for a Down Payment

Before 1956, down payments needed to be 20% of the home’s sale price. In 1956, banks adjusted their regulations, permitting homebuyers to make down payments of less than 20%. There was a crucial condition attached to this change. Those who used this option would be required to make an extra monthly payment called private mortgage insurance (PMI). Essentially, PMI serves as a safeguard for the bank in case of default by the borrower. While 20% is not a requirement today, in fact, there are loan options as low as 0 down, there are significant advantages to putting 20% or more down.

Putting 20% down eliminates the requirement for the PMI fee, keeping more money in your pockets. Even more so, making a down payment of 20% or more distinguishes your offer. Doing so, makes it more attractive to sellers and potentially enables you to secure a reduced interest rate for your mortgage through negotiation.

Finally, the more money you put down upfront reduces your monthly mortgage payment and the overall amount of interest you will pay. This keeps even more money in your pocket.

Set aside funds each paycheck

Consider saving by earmarking a portion of each paycheck to bolster your down payment fund. You can steadily accumulate funds over time by setting a clear savings goal and allocating a consistent amount from each pay period. If you prefer a more structured approach, consider opening a separate savings account dedicated solely to your down payment savings. Sometimes, you yield higher interest rates with a savings account.

Explore alternative avenues to boost your income

If you have skills or interests beyond your primary job, consider seeking part-time or freelance opportunities to generate additional revenue. You can expedite your journey toward homeownership by channeling this extra income directly into your down payment fund.

Review your current spending habits

Commit to reducing excessive spending. Perhaps commit to one less meal out a week, make your coffee at home instead of from the coffee shop, or skip out on the big vacation this year to increase your down payment. Consider using one of the many money management apps like Rocket Money to help you with your spending and saving goals.

Increase Your Credit Score

Your credit score is a factor considered when applying for a mortgage. A higher credit score maximizes your purchasing potential by potentially reducing your interest rate. The lower your rate, the more purchasing power you have.

To boost your credit score, prioritize paying down outstanding balances on your credit cards. Prioritize those with high-interest rates. Avoid opening unnecessary new lines of credit and steer clear of significant purchases leading up to the period when you’re ready to make a home offer. Remember that student loans also affect your financial profile, so consistently making payments will enhance your overall credibility with lenders.

Reduce Your Debit-To-Income Ratio

Lenders not only look at your creditworthiness, but they also consider your debt-to-income ratio. How much money do you owe vs. how much you make. This is important because you must be able to afford the home you are buying, pay off your current debts, and have enough money for day-to-day living.

The front-end ratio

Lenders assess your ability to repay a mortgage by examining your housing ratio. This ratio represents the percentage of your monthly gross income that will be allocated to your mortgage payment. It is calculated by dividing your monthly mortgage payment by your monthly gross income. A higher ratio indicates a greater risk of default.

The back-end ratio

The back-end ratio plays a crucial role in assessing your financial health. It gauges the percentage of your monthly income allocated to debt repayment. Included in this calculation is mortgage payments, credit card bills, student loans, and other loan obligations. It is calculated by dividing your total monthly debt expenses by your gross monthly income. This ratio offers insight into your ability to manage debt responsibly and affects your loan eligibility.

Increasing your credit score, reducing credit card balances, and making regular, on-time payments toward your loans contribute to lowering your overall debt while enhancing your debt-to-income ratios. This positive financial behavior demonstrates your ability to manage debt responsibly. In turn, it strengthens your financial position and enhances your buying power.

These key factors are not the only aspects of purchasing a home but they play a significant role. We strongly suggest speaking to a trusted lender early on to get specific recommendations based on your unique financial situation. Remember, increasing your buying power is a lengthy process. Having a specific strategy is key to staying on track. Make an attainable plan so that when your dream home comes along, you are in the best financial position to make it your reality.

Connect with us to get the conversation started.

Set Yourself up for Success by Doing These 7 Things When Buying Your First Home

Buying your first home can be easy when you are adequately prepared and you have a good agent on your side. But where to start and what actions are most important? We will get you pointed in the right direction. Let’s get started!

-

Know your credit score.

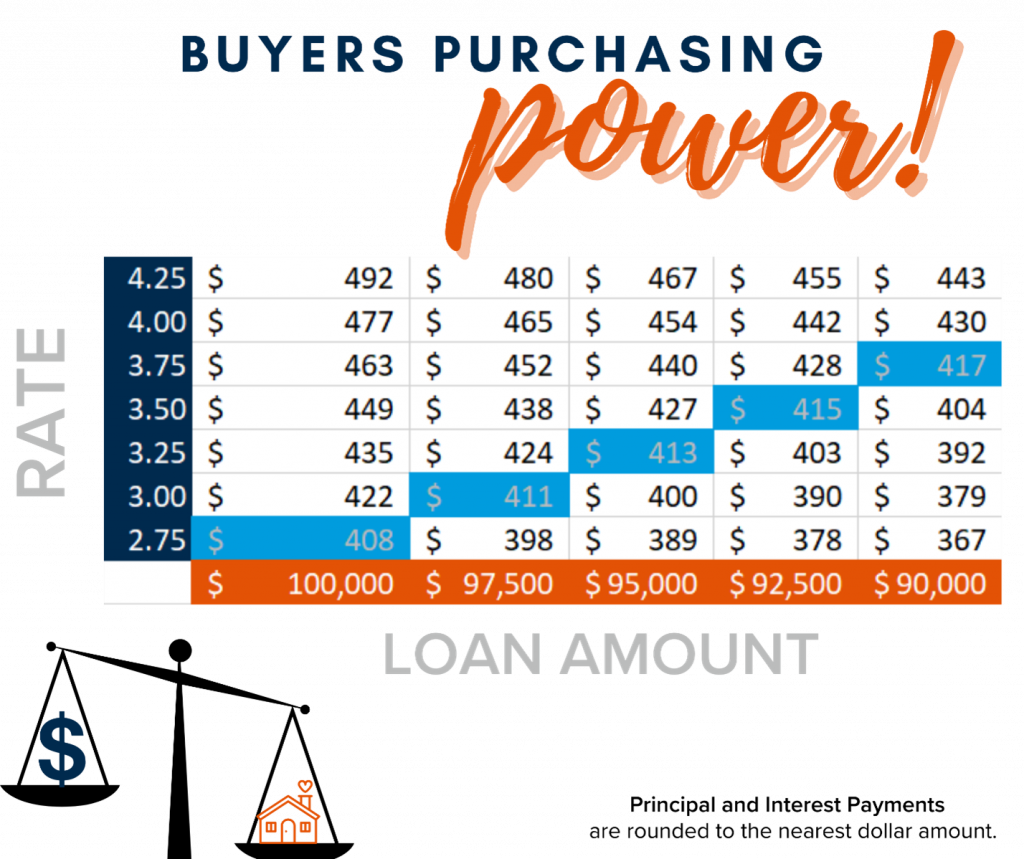

Many first-time homebuyers fail to recognize that one of the most important factors in getting approved for a mortgage is their credit score. The health of the score determines not only the interest rate but also whether they will be approved for a mortgage in the first place. Some people wonder why the interest rate really matters. The truth is that the slightest difference in rate can mean big money over 30 years! As the chart below demonstrates, a lower interest rate helps buyers afford a higher-priced house and still pay less monthly. Check out this article to learn more about Credit score rankings and what they mean.

-

Set a clear budget and stick with it.

Another big mistake first-time homebuyers make is not budgeting realistically and then finding out they cannot really afford the house they chose. A great way to get an idea of how much you should realistically spend on a mortgage is to determine your debt-to-income ratio. This number can be calculated by adding all your monthly debt payments (mortgage, credit card bill, car payment, etc.) together and then dividing by the gross monthly income. A conservative percentage of your income spent paying down debt would be 20-25%, a medium would be 25-30%, and a high would be 30-38% (or higher when using gross income vs. net).

-

Remember there are other fees other than the mortgage payment.

Homeownership comes with fees and other bills that you may not have as a renter. In addition to principal and interest on the mortgage payment, there will be real estate taxes and homeowner’s insurance. Check to see if the home is part of a homeowner’s association as there may be annual or monthly dues for that (a great agent will let you know about this). These fees typically show up as part of the mortgage payment. However, what is often forgotten or inaccurately calculated is the utility bills like water, sewage (or septic inspections/pumping), garbage, and energy bills. Furthermore, unlike renting if a pipe breaks or roof leaks there is no maintenance man that just shows up to repair it. Remember to budget for the maintenance of the home. This includes mowing the lawn… do you have a lawnmower yet?

-

Leave a cushion.

As discussed, buying a home has a lot of upfront costs. A bank account that seemingly had a plethora of cash can quickly be drained after the down payment, closing costs, moving expenses, and furnishing a new home. Having a healthy emergency fund is so critical as a homeowner.

Check out this helpful article by Dave Ramsey.

-

Once steps 1-3 are completed get pre-approved.

Don’t just meet with any lender, be sure to find a highly reputable local lender that the top listing brokers recommend (this will give you a competitive advantage). Not only does the pre-approval give buyers a realistic idea of how much they can borrow, but it can also be the defining factor of whether or not they get the home. Let us explain. A pre-approval speeds up the process and demonstrates the person is a serious buyer, not just a lookie-loo. When it comes down to multiple offer situations, as we see so frequently now, it is critical to have the most well-presented offer. Showing the seller that you are not only serious but that you have been pre-approved for the funds needed to buy with a lender they respect sends a strong message that you are the one the seller should choose! Check out our local lenders here.

-

Ask questions about your options!

Not everyone’s situation is the same. Similarly, loans are uniquely created to fit individual needs. Historically, it has been thought that buyers need to come to the table with at least a 25% down payment. Today that is just not true. While it is always good to have money for your mortgage down payment, there can be alternative options if you don’t. VA mortgages can be secured for 0% down and conventional mortgages for as little as 3%. Check out these different mortgage types meant to uniquely fit your life.

-

Hold off on any spending spree and do not take out a line of credit.

Remember that “debt-to-income ratio” mentioned above? Your mortgage approval is linked heavily to this number. This is not the time to go out and buy a new sportscar, purchases new appliances, and or upgrade your electronics. Borrowing money after getting pre-approved increases the debt-to-income ratio, and this will be re-checked just prior to the loan being approved. Applying for a new loan or credit card will also likely decrease your credit score. If either of these things happen prior to closing it could mean losing the mortgage and the interest rate you locked in. So, hold off on spending or even giving out your social security number to anyone!

We hope this helps point you in the right direction. We would love to be your guide as you prepare and navigate the path to homeownership! Call us today and we can connect you with an expert Buyers Broker! 360.675.5953.

If you enjoyed this you might also like:

5 Most Affordable Neighborhoods Near Oak Harbor & NAS Whidbey