Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Maximizing Your Purchasing Potential

When it comes to purchasing a home, understanding your buying power and strategically taking steps to enhance your position are key to maximizing your purchasing potential. Beyond just envisioning your dream home, it is crucial to recognize the numerical factors lenders consider when approving you for a mortgage. By strengthening the following key areas, you can elevate your financial standing and position and find success in a competitive housing market.

Strategies to Maximize Your Purchasing Potential

First and foremost, give yourself time to prepare. Change will not happen overnight. Be patient and give yourself grace. Create a list of attainable goals and make consistent efforts to reach them. Over time, you will see the difference. We suggest talking to a lender as soon as possible so they can help identify specific key areas unique to you. Overall, you can increase your buying power by preparing for a down payment, increasing your credit score, and reducing your debit-to-income ratio.

Prepare for a Down Payment

Before 1956, down payments needed to be 20% of the home’s sale price. In 1956, banks adjusted their regulations, permitting homebuyers to make down payments of less than 20%. There was a crucial condition attached to this change. Those who used this option would be required to make an extra monthly payment called private mortgage insurance (PMI). Essentially, PMI serves as a safeguard for the bank in case of default by the borrower. While 20% is not a requirement today, in fact, there are loan options as low as 0 down, there are significant advantages to putting 20% or more down.

Putting 20% down eliminates the requirement for the PMI fee, keeping more money in your pockets. Even more so, making a down payment of 20% or more distinguishes your offer. Doing so, makes it more attractive to sellers and potentially enables you to secure a reduced interest rate for your mortgage through negotiation.

Finally, the more money you put down upfront reduces your monthly mortgage payment and the overall amount of interest you will pay. This keeps even more money in your pocket.

Set aside funds each paycheck

Consider saving by earmarking a portion of each paycheck to bolster your down payment fund. You can steadily accumulate funds over time by setting a clear savings goal and allocating a consistent amount from each pay period. If you prefer a more structured approach, consider opening a separate savings account dedicated solely to your down payment savings. Sometimes, you yield higher interest rates with a savings account.

Explore alternative avenues to boost your income

If you have skills or interests beyond your primary job, consider seeking part-time or freelance opportunities to generate additional revenue. You can expedite your journey toward homeownership by channeling this extra income directly into your down payment fund.

Review your current spending habits

Commit to reducing excessive spending. Perhaps commit to one less meal out a week, make your coffee at home instead of from the coffee shop, or skip out on the big vacation this year to increase your down payment. Consider using one of the many money management apps like Rocket Money to help you with your spending and saving goals.

Increase Your Credit Score

Your credit score is a factor considered when applying for a mortgage. A higher credit score maximizes your purchasing potential by potentially reducing your interest rate. The lower your rate, the more purchasing power you have.

To boost your credit score, prioritize paying down outstanding balances on your credit cards. Prioritize those with high-interest rates. Avoid opening unnecessary new lines of credit and steer clear of significant purchases leading up to the period when you’re ready to make a home offer. Remember that student loans also affect your financial profile, so consistently making payments will enhance your overall credibility with lenders.

Reduce Your Debit-To-Income Ratio

Lenders not only look at your creditworthiness, but they also consider your debt-to-income ratio. How much money do you owe vs. how much you make. This is important because you must be able to afford the home you are buying, pay off your current debts, and have enough money for day-to-day living.

The front-end ratio

Lenders assess your ability to repay a mortgage by examining your housing ratio. This ratio represents the percentage of your monthly gross income that will be allocated to your mortgage payment. It is calculated by dividing your monthly mortgage payment by your monthly gross income. A higher ratio indicates a greater risk of default.

The back-end ratio

The back-end ratio plays a crucial role in assessing your financial health. It gauges the percentage of your monthly income allocated to debt repayment. Included in this calculation is mortgage payments, credit card bills, student loans, and other loan obligations. It is calculated by dividing your total monthly debt expenses by your gross monthly income. This ratio offers insight into your ability to manage debt responsibly and affects your loan eligibility.

Increasing your credit score, reducing credit card balances, and making regular, on-time payments toward your loans contribute to lowering your overall debt while enhancing your debt-to-income ratios. This positive financial behavior demonstrates your ability to manage debt responsibly. In turn, it strengthens your financial position and enhances your buying power.

These key factors are not the only aspects of purchasing a home but they play a significant role. We strongly suggest speaking to a trusted lender early on to get specific recommendations based on your unique financial situation. Remember, increasing your buying power is a lengthy process. Having a specific strategy is key to staying on track. Make an attainable plan so that when your dream home comes along, you are in the best financial position to make it your reality.

Connect with us to get the conversation started.

Mortgage Rate Predictions and Misconceptions

Written by Matthew Gardner

The Federal Reserve Bank of New York just released their 2023 Housing Survey, which shows how the U.S. population feels about the housing market. Windermere Chief Economist Matthew Gardner digs into the mortgage rate predictions, showing how demographics played a role in the results.

This video on mortgage rate predictions is the latest in our Monday with Matthew series with Windermere Chief Economist Matthew Gardner. Each month, he analyzes the most up-to-date U.S. housing data to keep you well-informed about what’s going on in the real estate market.

Mortgage Rate Predictions

Hello there! I’m Windermere Real Estate’s Chief Economist Matthew Gardner. This month we’re going to take a look at the latest SCE Housing Survey, which gives us a really detailed look at consumers’ psyche in regard to the housing market.

I’ve always been fascinated by surveys, as they frequently give me insights that I simply don’t get from just looking at raw data and, as luck would have it, the New York Fed just released its 2023 Consumer Expectations Housing Survey. Now, this particular survey has always given me some great and often surprising insights as to how the U.S. population views the overall housing market. We certainly don’t have time to cover all of the questions that the survey poses, but there was one section I wanted to share with you today as it really resonated with me, and it relates to mortgage rates.

Will mortgage rates continue to rise?

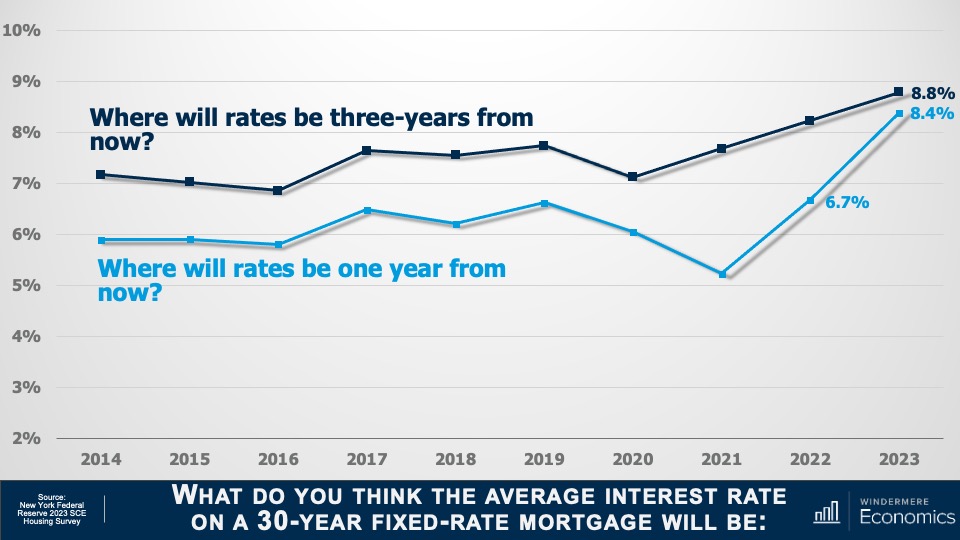

The first question asked was where they expected mortgage rates to be one year from now. And as you see here that, on average, households expected rates to rise all the way up to 8.4%. Although some may see this as extreme, you can see that in the 2022 survey respondents predicted rates would hit 6.7%, almost exactly where they were at the beginning of this March.

And when asked where they thought rates would be three years from now, on average, households expected to see them climb to 8.8%. Now, that’s a rate we haven’t seen since early 1995!

Well, I’m not sure about you, but I was very surprised by these results as they counter just about every analyst’s expectation regarding where rates will be over the next few years. In fact, myself and every economist I know believes that rates will slowly pull back as we move through this year. I haven’t seen a single forecast suggesting that mortgage rates will rise to a level this country hasn’t seen in decades.

But as they say, the devil’s in the details. When I dug deeper into the numbers, it became very clear to me that demographics played a pretty big part in guiding people’s answers. Let me explain.

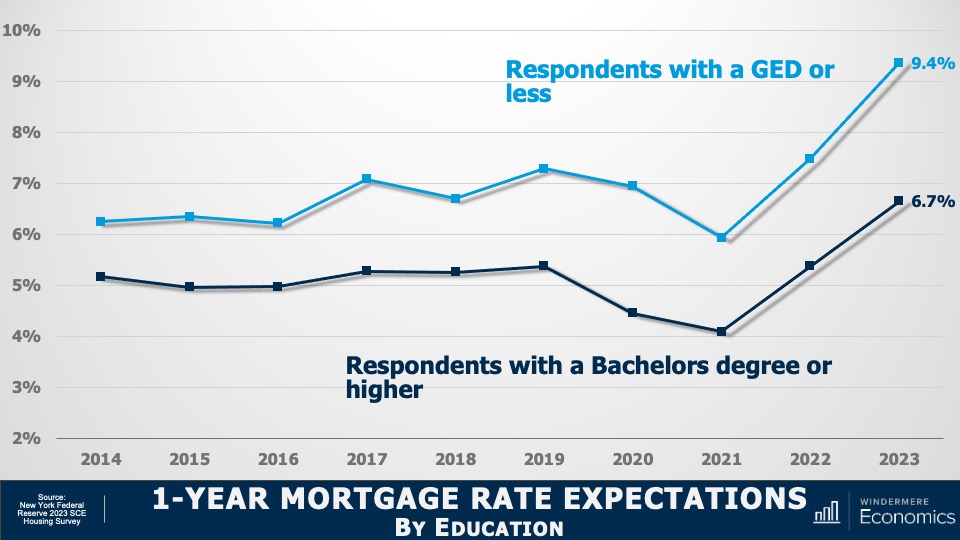

1-Year Mortgage Rate Expectations by Education

Here the data is broken down by educational achievement. You can see that survey respondents who didn’t have a college degree thought that mortgage rates would rise to 9.4% within a year. But college graduates were far more optimistic, and they expected rates to be in the high 6’s.

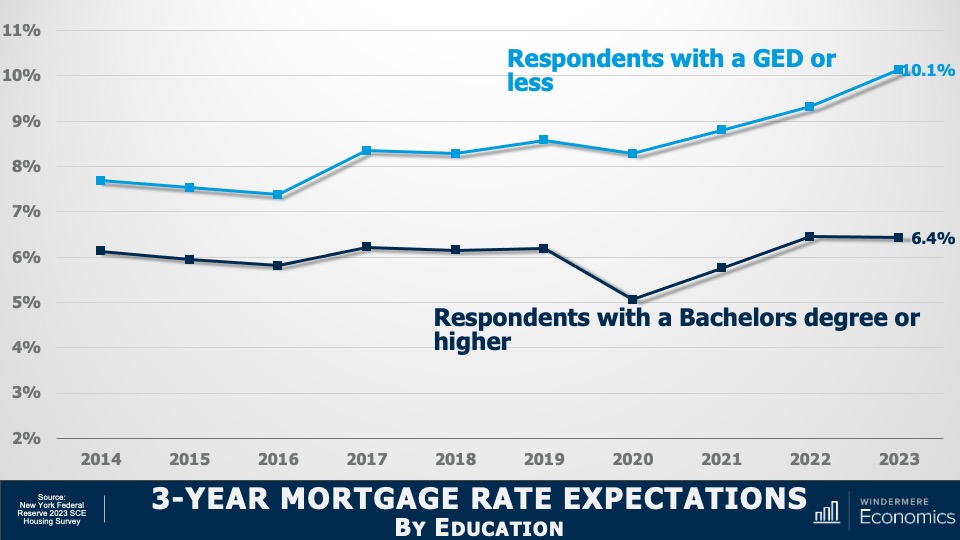

3-Year Mortgage Rate Expectations by Education

And when asked to look three years out, respondents without degrees expected rates to break above 10%. While college graduates saw them pulling back a little from their one-year expectations of 6.7%, down to 6.4%.

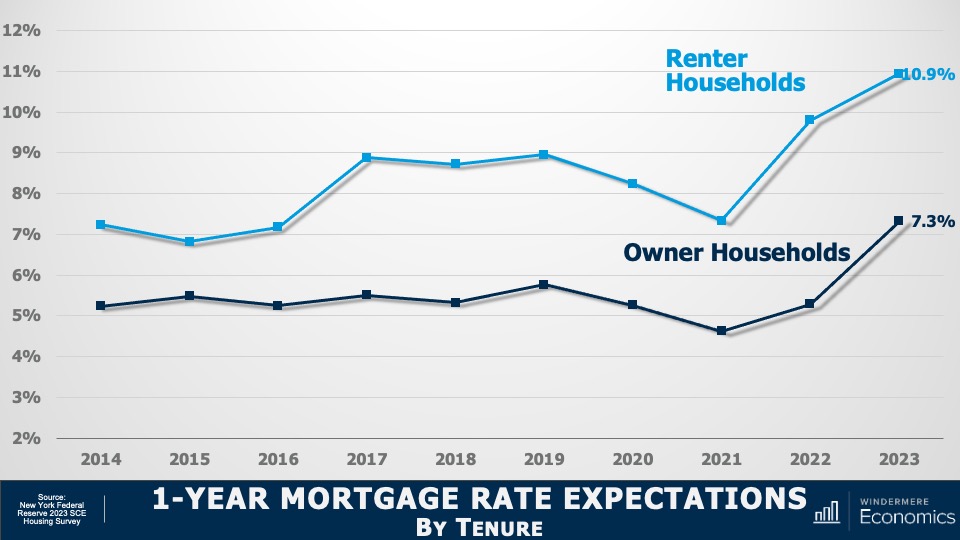

Now we are going to look at the survey results broken down by housing tenure.

1-Year Mortgage Rate Expectations by Tenure

And here you see that renters expect mortgage rates to be at almost 11% within a year. And homeowners also saw them rising, but only up to 7.3%.

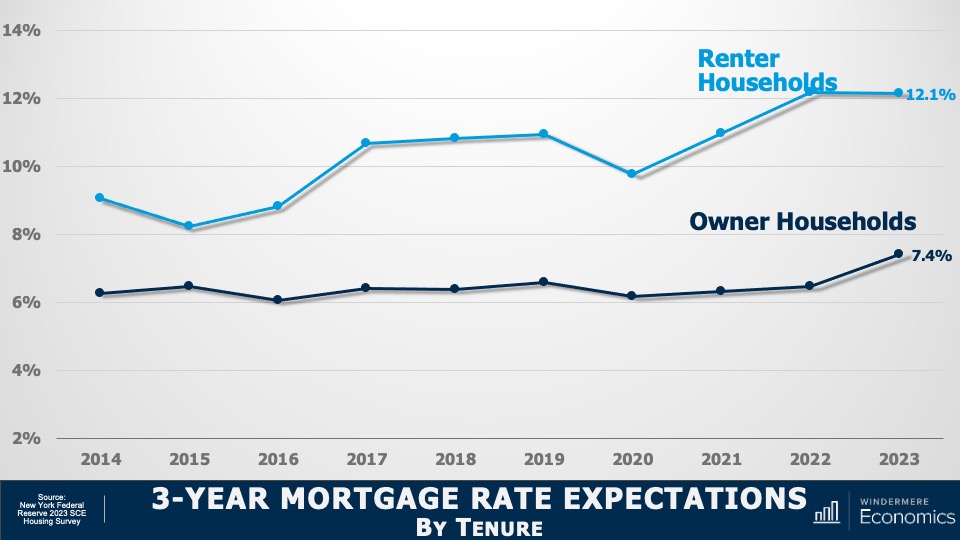

3-Year Mortgage Rate Expectations by Tenure

And over the next three years, renters expected rates to break above 12%. That’s a level not seen since the fall of 1985. But homeowners expected to see rates at a somewhat more modest 7.4%.

So, what does this tell us? I see two things.

Firstly, the rapid increase in mortgage rates that we all saw starting in early 2022 has a lot of people believing that we will see rates continuing to rise, sometimes at a very fast pace, over the next few years. I mean, if it happened before, why can’t it happen again? And this mindset leads me to my second point, which is that it’s very clear that a lot of would-be home buyers just don’t understand how mortgage rates are calculated.

The bottom line here is that I see a potential buyer pool out there that needs educating and that can give an opportunity to brokers to discuss how rates are set and where the market is expecting to see them going forward.

This may alleviate the concerns that many households have who may be thinking that they will never be able to afford to buy a home because of where they expect borrowing costs to be in the future. Education is everything, don’t you agree?

As always, I’d love to get your thoughts on this topic so please comment below! Until next month, take care and I will see you all soon. Bye now.

To see the latest housing data for your area, visit our quarterly Market Updates page.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

If you have further questions and would like to discuss with a Realtor connect with us here.

Expedite the Loan Process

Knowing what to expect not only calms your nerves but also expedites the lending process.

During your search for a lender, you will discover that most lenders will sincerely work on your behalf to help you attain the financing needed to quickly get you into the home you have chosen.

Your chosen lender will guide you through the process and shed light on the documents you need to prepare as well as provide you with the various options available to you. Talking to a lender well in advance about your goals and your financial situation will better prepare you for home ownership. The journey is different for everyone. We cannot stress enough how important it is to talk to a lender early on. The lender can help you determine a realistic timeline and address any problems early on to prevent a problem from arising later that could cost you your dream home.

To expedite the loan process come prepared with the following documentation.

- Your most recent pay stubs (this should be computer generated and include the YTD earnings and deductions).

- Last two years’ W2s.

- Two years’ tax returns.

- Copy of your valid U.S. picture ID (bring the ID with you)

- Two months’ bank statements for all your accounts (must include the date, name, and account numbers)

- Last two statements for asset accounts such as IRA, 401K, investment, ect.

- Contact information for whom you anticipate getting your home insurance. (Connect with us if you need help finding home insurance companies)

- If applicable, bankruptcy documentation including discharge paperwork

- If applicable, a divorce decree and/or child support court order

What if I’m self-employed?

If you are self-employed it is of the utmost importance for you to speak with a lender as soon as possible if homeownership is on your wish list.

You will need to come prepared with things like the last two years of Business Tax Returns and if possible, a letter from your CPA detailing at the very least two years of self-employment with a continued positive outlook for your business.

To help you get started with your search check out Guild Mortgage, Peoples Bank, and Home Bridge for a few lenders here on Whidbey Island. Don’t forget to check out our Neighborhood Guide when you are ready to start looking for your dream home on Whidbey.

We hope this was of help to you. If you need help connecting with a lender, send us a message here. If you are ready to start speaking to an agent about the next steps let us know you are ready to start looking in a message to us here.