Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Spring Cleaning

Spring cleaning has long been a cherished tradition embraced by households worldwide. Stemming from a practical need to freshen up living spaces after the long winter months, this annual ritual has evolved into a symbol of renewal and rejuvenation. Beyond simply tidying up, spring cleaning holds significant importance for both physical and mental well-being. By clearing out clutter, dust, and grime accumulated over the winter, we create a cleaner and healthier environment for ourselves and our families. Moreover, the act of spring cleaning can have positive effects on our mindset, providing a sense of accomplishment, satisfaction, and a renewed energy to tackle new challenges. Embracing this tradition allows us to start the new season on a clean slate, fostering a sense of optimism and positivity as we welcome the warmer days ahead.

Follow along for a comprehensive spring cleaning checklist to help you tackle every corner of your home:

Declutter and Donate

- Make your home more inviting by decluttering. Go through each room and declutter by getting rid of items you no longer need or use.

- Donate, sell, or discard items that are no longer serving a purpose for you. Consign your items at places like My Sisters Closet, or host a yard sale and feel a sense of accomplishment when you can fund something new. Whatever you find yourself still left with donate to a local thrift store. Island Thrift, WAIF Thrift Shop , and Treasure Island-Antique and Thrift are just a few of the many options on Whidbey Island.

Dust

- Open your windows and breathe a breath of fresh air.

- Dust all surfaces, including shelves, countertops, furniture, and electronics.

- Don’t forget to dust ceiling fans, light fixtures, and vents.

Clean Windows

- Spring brings so much outside beauty. Make sure you can enjoy it all with sparkling windows.

- Wash windows inside and out, including the window frames and sills. If your window has weeping holes, be sure to make sure they are not clogged so that excess water can drain properly.

- If cleaning your windows is out of reach there are companies like A Clean Streak or Oh Say Can You See that can help.

- Clean blinds, curtains, or drapes according to manufacturer’s instructions.

Vacuum and Clean Floors

- Vacuum carpets and area rugs thoroughly.

- Sweep and mop hard floors, paying special attention to corners and baseboards.

Deep Clean Kitchen and Restrooms

- Clean and disinfect countertops, cabinets, and drawers, all bathroom surfaces, including sinks, toilets, and tubs/showers.

- Clean appliances inside and out, including the refrigerator, oven, microwave, and dishwasher.

- Degrease stove hood and filter.

- Scrub tile grout and remove any mold or mildew.

Organize Closets and Cabinets

- Out with the old and in with the new… or maybe just move the sweaters to the back (we are still in the PNW and occasionally will still need those sweaters), but break out the vibrant tank tops it is spring already!

- Declutter and organize closets and cabinets, donating or discarding items as needed.

- Use storage bins or baskets to keep items organized and easily accessible.

Freshen up Bedding

- Launder bedding, including sheets, pillowcases, and duvet covers.

- To increase the life of your mattress, rotate and flip it for even wear.

Clean Upholstery and Furniture

- Vacuum upholstery and cushions to remove dust and debris. Make sure you get behind and underneath.

- Spot clean stains and spills on furniture.

Tidy Outdoor Spaces

- Sweep or pressure wash outdoor patios, decks, and walkways.

- Clean outdoor furniture and cushions.

- Trim bushes, trees, and clean up garden beds.

Inspect and Maintain

- Ensure your families safety every season.

- Check smoke detectors and carbon monoxide detectors, replacing batteries as needed.

- Test and clean ceiling fans.

- Schedule routine maintenance for HVAC systems, plumbing, and electrical systems.

Final Touches

- Brings some of the outside in.

- Add finishing touches such as fresh flowers or plants to bring life into your space.

- Sit back, relax, and enjoy your freshly cleaned and organized home!

Spring cleaning isn’t just about tidying up—it’s also an essential part of home maintenance and preparation for the warmer months ahead. For homeowners, it’s an opportunity to refresh their living spaces and ensure that their property is in top condition. Beyond the aesthetic benefits, a thorough spring cleaning can enhance the value of a home by improving its curb appeal and overall appeal to potential buyers. By decluttering, organizing, and performing deep cleaning tasks, homeowners can showcase their property’s full potential and make a positive impression on prospective buyers. Additionally, addressing maintenance issues early can help prevent costly repairs down the line and contribute to the long-term health and durability of the home. So, as spring approaches, embrace the tradition of spring cleaning as a valuable investment in both your home and your well-being.

If you are considering selling this Spring, connect with us.

To help get you motivated listen to our Spring Cleaning Playlist Here.

The Importance of Escrow in Real Estate Transactions

Real estate transactions can be complex and involve a considerable amount of money. Whether you are a buyer or a seller, real estate is often your biggest investment. That is why it is important for both buyers and sellers to protect their interests and ensure that the transaction is completed smoothly. This is where escrow comes in.

What is Escrow?

Escrow is a financial arrangement where a third party holds and regulates the payment of funds required for both the buyer(s) and the seller(s) involved in a transaction. Escrow helps ensure that the transaction is completed smoothly and according to the terms agreed upon by both parties. Both the buyer and the seller provide the escrow agent with written instructions. When all conditions have been met, the escrow officer sends the closing papers to the county recording office, where the new deed is recorded. The escrow officer then releases funds to the seller.

How is Escrow Used in Real Estate Transactions?

In a real estate transaction, escrow is used to ensure that the buyer’s funds are securely held until all the terms of the sale, such as the transfer of the property title, have been completed. In addition, the escrow agent may also be responsible for completing tasks such as ordering a title search, obtaining necessary documentation, and disbursing funds according to the instructions of the parties involved in the transaction. During this process you may hear the term title insurance and you might wonder what it is. Title insurance is like a safety net around your property. Sometimes hidden mistakes in previous deeds, mortgages, easements or other recorded documents might give someone else an ownership stake in the property. It is important for you to get Title Insurance to protect you and your home as it will save you time and money in the future if problems arise. You can learn more about it in our “What is title insurance and why is it important?” blog. Read it here.

In conclusion

Escrow is an important tool that helps to protect the interests of both buyers and sellers in a real estate transaction. It ensures that the transaction is completed smoothly and according to the agreed upon terms, and helps to reduce the risk of disputes or issues arising. If you are buying or selling a property, it is important for you to understand the role of escrow and how it can benefit you.

If you are ready to connect with an agent or have any further questions, please don’t hesitate to connect with us today by clicking here. If you are just getting started on your home buying journey, consider reviewing these real estate terms to help you along the way.

What is an Interest Rate Lock?

It is no surprise that you might have questions when buying a home. There is a lot to know. Having a good realtor on your side can help you navigate some of those tough questions. Don’t have a realtor of your own? Contact us here and we will get you connected.

In this article, we will be discussing mortgage loan rate locks and how they are used to help you when you are buying a home.

In a market with frequently changing interest rates, some people worry that their interest rate will change before they get into their homes. Depending on the individual circumstances this could be a realistic fear. It is important to discuss this with your trusted realtor and your lender. However, lenders know you need time to search for your home after you have been pre-approved. A rate lock is implemented to protect your agreed-upon rate for a specific length of time.

Let’s discuss this further.

A rate lock is an agreement between you and your lender guaranteeing a specific interest rate will be provided to you for a specific length of time after the pre-approval. This is called the rate lock period. Your lender will confirm with you your interest rate, the start date, and the date of expiration.

What if interest rates go up before I close on a house?

Rest assured you are locked in at your agreed-upon rate even if interest rates have gone up before you close. But again it depends on the expiration date. You might be wondering how lenders can do this. As soon as your rate is locked, lenders purchase money from their investors for you at your rate to be ready for you to spend it when you find your home. Assuming your loan application is approved (see our “Nervous about getting approved for a home loan?” article) and all the terms and conditions for the approval have been met the money is made available to you at closing regardless of the changes in the market after you had locked in your rate. Lenders do not ask you to pay a higher interest rate just because market rates have shifted upward.

Why you shouldn’t wait to lock your rate even when interest rates are dropping.

Would it be more disappointing to have locked in a rate and find that you have missed a lower rate, or NOT locking in your rate and then having rates increase? Trying to time the market can be a dangerous game. Often the market spikes without warning leaving buyers regretting not locking in lower rates. Don’t forget if rates continue to fall, you can often refinance your loan typically after 120 days. Check your lender’s post-closing refinancing policy and make sure to discuss this with your lender ahead of time.

If you do not have a lender of your own or would like to discuss buying or selling a home, please do not hesitate to connect with us so that we can help you.

Email us at WhidbeyCommunications@windermere.com or call us at 360.675.5953

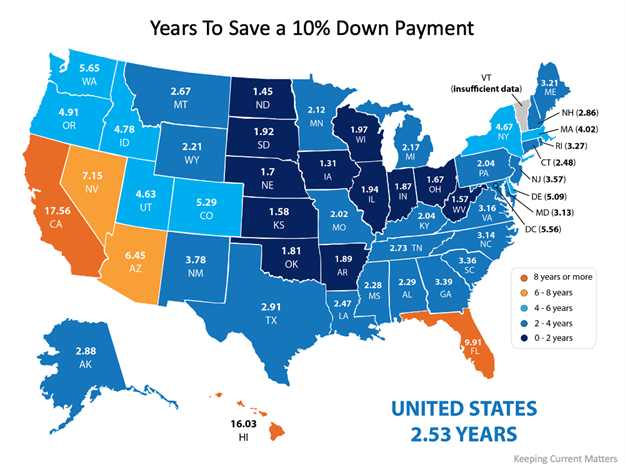

How Long Does it Take to Save For a Down Payment?

Saving enough money for a down payment on your first home can be one of the biggest obstacles to homeownership. Depending on your circumstance you might need anywhere from 3% – 20%. Speaking with a reputable local lender will help you find out exactly what your percentage will be.

But how long should it take, you ask!?

Follow along as we estimate the amount of time it takes a person earning a median income and paying a median rent to save up for a down payment on a median-priced home.

To accomplish this task we use the concept that homeowners should pay no more than 28% of their total monthly income on housing expenses. We use this information in combination with data from the U.S. Department of Housing, Urban Development (HUD), and Apartment List to determine our estimation.

According to the data pulled, the national average for the time it would take to save for a 10% down payment is roughly two and a half years (2.53). Looking at the diagram below you can also see that those living in Iowa can save for a down payment in as little as 1.31 years while those in California could take 17.56 years. The map below can help you determine the amount of time (in years) it can take for you to save in your state:

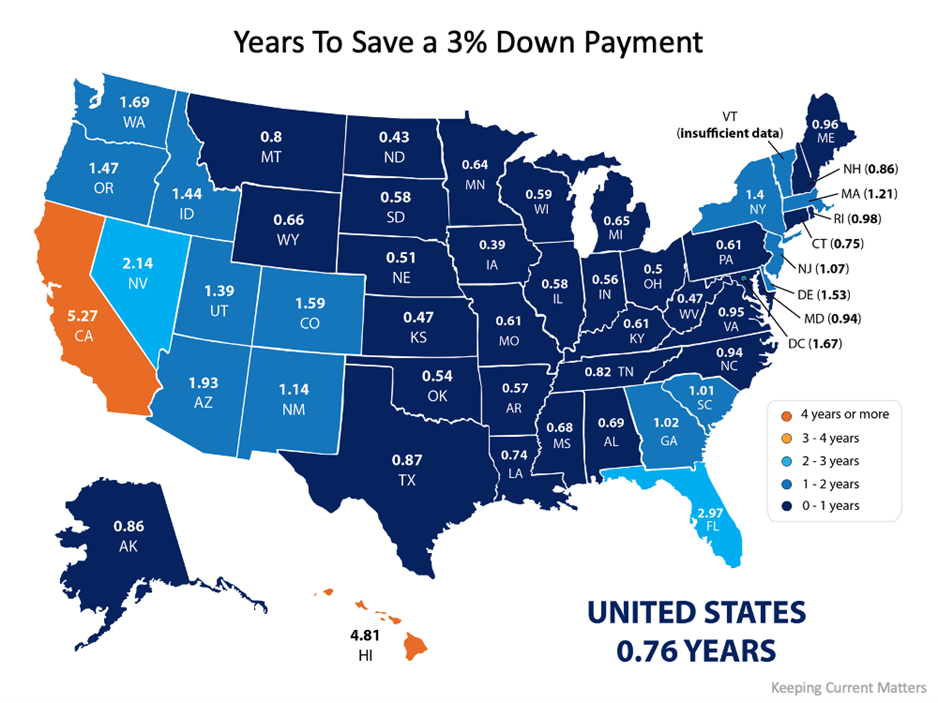

What if you only need to have a 3% down payment?

It is a common misconception that you need to have a 20% down payment to buy a home.

The reality is there are reasonable alternative options out there. First-time home buyers have an advantage with a plethora of down payment assistance programs available to them. You just have to find the right lender and ask. Need help finding a lender? Ask us to connect you with one here.

What if you qualify to take advantage of one of the 3% down payment programs?

If you qualify for a 3% down payment program, then you only have to come up with 3% of the total cost of the home at closing instead of ten or the typical 20% we have seen required in the past. Saving for a 3% down payment might not take you very long. In fact, it could take less than a year in most states, as shown in this map here:

At the end of the day

Wherever you are in the process of saving for a down payment, you may be closer to your dream home than you think. Connect with us to explore the options available to you in our area and how they support your plans for buying a home.