Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What is an Interest Rate Lock?

It is no surprise that you might have questions when buying a home. There is a lot to know. Having a good realtor on your side can help you navigate some of those tough questions. Don’t have a realtor of your own? Contact us here and we will get you connected.

In this article, we will be discussing mortgage loan rate locks and how they are used to help you when you are buying a home.

In a market with frequently changing interest rates, some people worry that their interest rate will change before they get into their homes. Depending on the individual circumstances this could be a realistic fear. It is important to discuss this with your trusted realtor and your lender. However, lenders know you need time to search for your home after you have been pre-approved. A rate lock is implemented to protect your agreed-upon rate for a specific length of time.

Let’s discuss this further.

A rate lock is an agreement between you and your lender guaranteeing a specific interest rate will be provided to you for a specific length of time after the pre-approval. This is called the rate lock period. Your lender will confirm with you your interest rate, the start date, and the date of expiration.

What if interest rates go up before I close on a house?

Rest assured you are locked in at your agreed-upon rate even if interest rates have gone up before you close. But again it depends on the expiration date. You might be wondering how lenders can do this. As soon as your rate is locked, lenders purchase money from their investors for you at your rate to be ready for you to spend it when you find your home. Assuming your loan application is approved (see our “Nervous about getting approved for a home loan?” article) and all the terms and conditions for the approval have been met the money is made available to you at closing regardless of the changes in the market after you had locked in your rate. Lenders do not ask you to pay a higher interest rate just because market rates have shifted upward.

Why you shouldn’t wait to lock your rate even when interest rates are dropping.

Would it be more disappointing to have locked in a rate and find that you have missed a lower rate, or NOT locking in your rate and then having rates increase? Trying to time the market can be a dangerous game. Often the market spikes without warning leaving buyers regretting not locking in lower rates. Don’t forget if rates continue to fall, you can often refinance your loan typically after 120 days. Check your lender’s post-closing refinancing policy and make sure to discuss this with your lender ahead of time.

If you do not have a lender of your own or would like to discuss buying or selling a home, please do not hesitate to connect with us so that we can help you.

Email us at WhidbeyCommunications@windermere.com or call us at 360.675.5953

Rising Mortgage Rates

Whether you are thinking about buying or planning to sell, it is critical for you to understand the role mortgage rates play on buyers purchasing power, and sellers listing prices.

But first, some definitions…

Mortgage rates:

the rate of interest charged on a mortgage loan.

Buyers purchasing power:

the amount of home you can afford to buy and is within your financial reach.

Seller’s listing price:

The sales price of a property when put on the market.

How the fluctuation in mortgage rates affect the two:

Buyers:

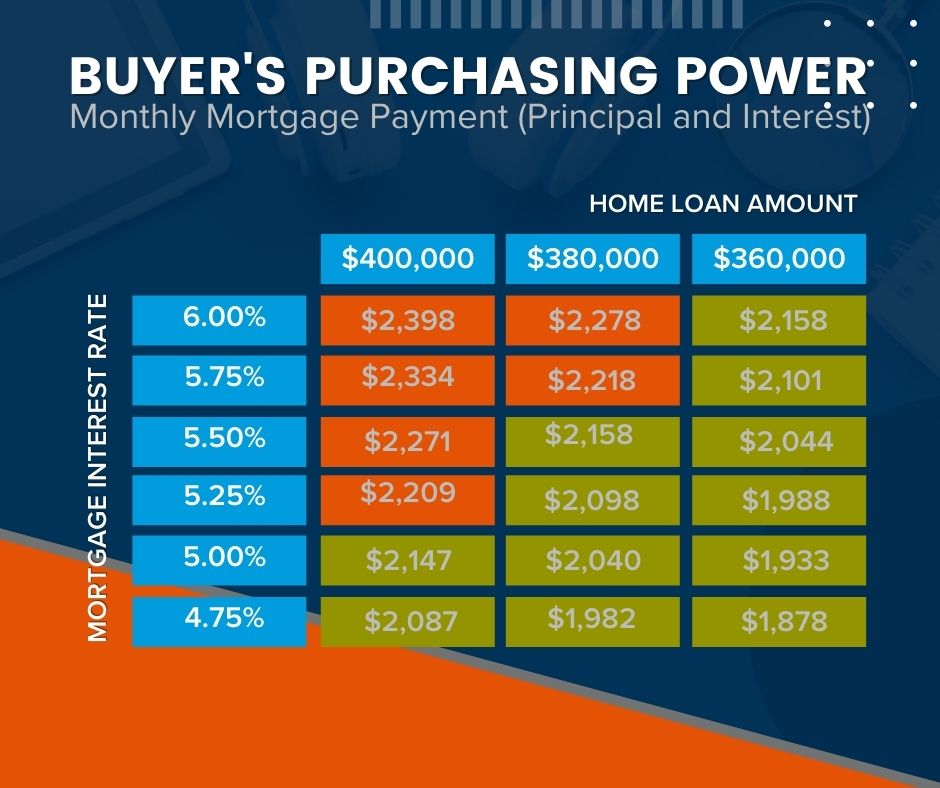

Mortgage rates directly affect the monthly payment buyers make on their home purchase. Even the smallest increases in mortgage rates can significantly impact their purchasing power. Typically speaking, for every 1% increase in mortgage rates buyers lose 10% of their purchasing power. In other words, when rates increase, so do monthly payments forcing many buyers to purchase less expensive homes to make up for the difference in interest and vice versa. With rates currently increasing, buyers need to beware that further mortgage rate increases could potentially limit their future purchasing power. If you are in the process of buying a home, it is of the utmost importance to have a strong plan. Connect with us so we can help you.

Sellers:

Rising mortgage rates result in a reduced number of overall buyers. With that said, we will likely begin to see the outrageous sales prices begin to decrease. Over the past couple years, we have witnessed a strong sellers’ market coupled with mortgage rates at an all-time low. This gave buyers the ability to purchase more home for low monthly payments. The limited inventory (homes for sale) resulted in wild selling prices. As buyers begin to get priced out of the market and mortgage rates begin to increase it will be of the utmost importance to carefully price your home for the market. You don’t want to risk coming out too high and getting stale or missing the opportunity to maximize interest. Skilled brokers will take into consideration and evaluate numerous factors when pricing expertly. It is not just the condition and location of the home, recent nearby sales, price of similar homes currently on the market but also mortgage rates, buying power, and other local variables. If you are thinking of selling connect with us so we can position your property to stand out in the current market.

Freddie Mac is saying. “History suggests that when rates rise, there is an initial bump in home prices, as many move quickly to buy a home before rates increase further. But after that period, home prices slow. Freddie Mac analysis shows that a 1% increase in mortgage rates results in home price appreciation that is four percentage points lower. For instance, a 1% increase in mortgage rates would change home price growth from 11% to 7%.”

Where we are at today:

Currently, the average 30-year fixed mortgage rate is above 5%. Experts anticipate that mortgage rates will continue to increase in the months ahead. If you are a buyer you have an opportunity to get in ahead of that increase by purchasing now.

Expert tip:

It is critical for you to get preapproved as early as possible to get todays rates locked in and prepare yourself with a plan incase rates are to go up. Additionally, sellers have a unique opportunity to still capitalize on the current situation if they are to list now before more buyers are completely priced out of the market and home prices are still strong. The graph below illustrates how mortgage interest rates drastically impact purchasing power and ultimately reducing the number of buyers bidding on homes in the higher price ranges.

Whether you are considering buying or selling let’s connect so that you have a trusted real estate advisor on your side who can help you strategize to achieve your dream of home ownership.