Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Perfect Time For You

The housing market is continuing to shift as inventory levels rise and buyers gain more options. If your home search was put on pause these past few years, you’re not alone. Luckily for you, there are options. Today’s current market might be the perfect time for you to resume looking. Let us explain why.

Currently we are seeing an increase in homes for buyers to choose from. In addition to the increase in inventory many buyers are noticing that prices have begun to level off in many areas. Pair increased inventory and leveling prices with mortgage rates that have begun to ease, and today’s market is currently the one many have been waiting for.

Continue reading for the breakdown.

Increased Inventory

With more homes coming onto the market and months of inventory increasing, we’re moving away from the highly competitive seller’s market we’ve experienced over the past several years. Buyers now have more choices, additional time to make decisions, greater negotiating power, and less competition with other buyers. Allowing buyers a more enjoyable purchasing experience and the ability to truly find their perfect home. While well-priced homes are still selling, the increase in available inventory is creating a more balanced market. A balanced market offers opportunities for both buyers and sellers.

Therefore, if you are selling, now more than ever it is of the utmost importance to have a trusted, professional realtor on your side. Your realtor can help position your property appropriately, be more strategic with pricing, and increase your homes presentation to stand out to get your home seen by potential buyers. Need a trusted realtor? Connect with us.

The Big Picture

The United States is experiencing more homes on the market compared to the same time last year. We know what you’re thinking. “Not every market is the same, and how does it compare to pre-covid numbers?”

In the South and the West inventory has fully recovered and in some places even surpassed pre-pandemic levels. However, supply remains tighter in much of the Northeast and Midwest where inventory is still below the historical normal. It is important to always discuss with your Realtor what the market looks like in your market.

More Choices Everywhere

Even with not every area fully recovered it is still a win for everyone. When you look at the bigger picture, inventory is up in every region. That means more choices everywhere, even though some areas have more homes for sale than others. With fewer buyers in the market and more homes for sale, sellers are willing to negotiate to get a deal done.

What’s happening in your area might look different than the national or regional trend. It’s important to work with a local Realtor that can help you understand your market and positioning. If you previously paused your home search this could be the time to take another look.

Maybe you’re still not ready. Connecting with your trusted Realtor now can help you prepare your budget, narrow your search, and make sure you fill prepped when the right home does show up on the market.

How Do I Sign My Closing Documents?

“How Do I Sign My Closing Documents If I’m Not Physically There?”

One of the most common questions buyers that are relocating, traveling, or purchasing from out of the area ask is: “How do I sign my closing documents if I can’t be there in person?”

The good news is that you do have options. The important part is understanding which documents can be signed remotely and which cannot.

Digital Signatures: What Can Be Done Online

Some of your closing documents can be signed electronically using platforms like DocuSign. These typically include disclosures and preliminary paperwork that don’t require notarization. Digital signing is convenient, fast, and often helps keep the process moving forward while you’re away.

Wet Signatures: What Must Be Signed in Person

Many final closing documents, especially those related to financing and the transfer of ownership, require a wet signature. This means they must be signed in ink and notarized. Traditionally, this is done at the escrow office, which is usually the simplest and smoothest option when you’re local.

When You Can’t Get to Escrow

If signing at the escrow office isn’t possible, there are alternatives:

-

Mobile Notaries:

A mobile notary can meet you at your home, office, hotel, or another agreed-upon location to complete the signing. This option offers flexibility but does come at an additional cost that is typically paid by the buyer and keep in mind that the fees can be $150 or more, depending on location and timing.

-

Buyers Overseas:

In some cases, when buyers are outside the United States, closings have been completed through a U.S. embassy or consulate. While this is possible, it often requires advance planning, availability, and strict scheduling.

Important Timing Considerations

It’s important to keep in mind that closing dates can be a moving target. When using a mobile notary or an embassy, appointments must be scheduled in advance. If timelines shift, rescheduling can be difficult and may lead to added stress or delays right at the finish line.

The Bottom Line

If you’re not physically present for closing, it doesn’t mean the transaction can’t move forward. However, it does mean planning ahead is critical. Each option comes with its own logistics, costs, and timing considerations. That’s why it’s always best to talk through your specific situation early, so we can choose the smoothest path and avoid last-minute headaches. It’s all manageable. Just start early if needed.

If you know you’ll be out of town or overseas during closing, let’s start the conversation early—I’m here to help coordinate the details and make the process as seamless as possible.

If you are thinking about buying and not currently working with an agent and would like to speak with one that understands this process and can help make it a smooth transition for you, connect with us!

Windermere E3

A reflection of our 2025 Windermere E3: Engage, Energize, Elevate event.

At Windermere, growth isn’t just about closing transactions. It is about elevating the experience for everyone involved, from our agents to our clients and communities. We grow together to better serve you. That spirit of growth and connection was at the heart of our recent Windermere E3 event held at the beautiful Suncadia in Cle Elum. Agents from across the region came together for a few unforgettable days of education, collaboration, and celebration.

Why being part of Windermere is so special

From networking to dancing the night away, the event was a vibrant reminder of what makes being a part of Windermere so special. Together we share a commitment to learning, supporting one another, and serving our clients with excellence.

Lead by the best in the industry to better serve you

Throughout the event, agents engaged in insightful sessions led by some of the best in the industry. Sharing strategies to enhance communication, improve client care, and stay ahead in a constantly evolving market. Every conversation, breakout session, and connection was focused on one goal: how to provide a better experience for the buyers and sellers we serve.

Supporting community needs

Beyond education, we also came together to give back. Together we raised $22,000 through live and silent auctions to support homeless families in need. It was a powerful example of how collaboration and compassion go hand in hand at Windermere.

When you work with a Windermere agent, you are not just working with a real estate professional. You are partnering with someone who is continually learning, evolving, and striving to deliver the highest level of service. Because when we engage, energize, and elevate each other, we elevate the entire experience of buying or selling a home.

A heartfelt thank you to everyone who made Windermere E3 possible. A special thank you to Shawna Ader for creating such an inspiring and impactful event.

At Windermere, we don’t just sell homes. We build relationships, strengthen communities, and continually push ourselves to be better for you.

If you are considering buying or selling and are in need of a real estate professional by your side, connect with us.

Home For The Holidays

Are you ready to make your dreams come true for the holidays? Let us help you get into a new home for the holidays.

The end of the year is quickly approaching!

Like many others, you are likely getting caught up in the hustle and bustle of the Holiday season, buying turkeys for Thanksgiving, prepping your Black Friday shopping list, and starting to think about a Christmas tree if you haven’t put it up already.

You might also be taking time to reflect on the past year to see if you have hit the mark on your goals and likely feeling a bit guilty for not quite reaching your 2022 New Years’ Resolutions.

We don’t blame you. Life gets busy. We understand that life has changed immensely for a lot of people in a short period of time. Many people are permanently working from home and are finding they need more space for organization to be successful. Maybe a new baby or puppy was added to the family and the rooms are feeling a bit cramped. Perhaps the cousin got married and now hosting holiday meals requires more space than you have. Don’t worry we can help.

If selling your home and getting into something bigger was part of your to-do list there is still time. In fact, now may be the best time.

Here’s why:

- When fewer homes hit the market the homes that do get the spotlight.

- While everyone else has Holidays on their mind, the serious buyers shop real estate and are significantly more motivated than any other time of year.

- This time of year offers the best staging opportunity to shine the best light on your listing.

- The equity you have gained in your present home can help you make the move into the home you’re dreaming of.

GET THE SPOTLIGHT

In residential real estate, it is quite normal to see fewer homes listed during the last couple of months of the year. Homeowners get busy around the holidays and put off selling their houses until the start of the new year when there is more time in their schedules and social calendars.

This creates an advantageous opportunity for those ready to sell now. While other homeowners are holding off until after the holidays, your home can soak up all the spotlight. If you are ready to start the process with a real estate professional today connect with us here.

SERIOUS BUYERS SHOP DURING THE HOLIDAYS

Your home might be exactly what that serious buyer has been waiting for, and sellers during this time will have less “looky loos” and more serious buyers.

When buyers’ demand is greater than the housing supply it is considered a Sellers’ Market which gives the seller the advantage.

If you work with an agent to list your house now, you’ll be able to get in front of enthusiastic buyers that are eager to make the move before the end of the year.

THE HOLIDAYS PRESENT A UNIQUE OPPORTUNITY

Have you ever looked in a magazine and wished you were living in its pictures? The same can happen with real estate photos. We know that listings that look more appealing online get people in their doors.

Warm fires in the fireplace and cookies baking in the oven can create that atmosphere that no other season seems to offer.

LEVERAGE THE EQUITY YOU HAVE FOR THE HOME OF YOUR DREAMS

If you have owned your home for several years, you likely have a large amount of equity (Total value minus what you owe.) This value can help springboard you into your next home. CoreLogic explained that the average equity per mortgage holder has rocketed to almost $300,000. Never has it been this high in history. The equity you have in your house right now could cover some, if not all, of a down payment on the home you have been dreaming of, and we can help get you in it.

If you are thinking about selling your house so you can find a home that better suits your needs, don’t delay your plans. Let’s connect so you can accomplish your goals before the end of the year. CLICK HERE.

You’ll Lose Money When You Overprice Your Home

You are probably asking yourself, “did I read that right?”

Yes, yes you did.

It is normal for sellers to want to get the most money out of the sale of their homes. It feels safe to list your home at the price you are desiring to get, but the reality is listing high might actually do your pocketbook more harm than good in the long run. Follow along as we explain why.

RISKS OF OVERPRICING YOUR HOME

You are drawing the attention of the wrong buyers.

Most people begin their home purchasing journey by searching which homes are available in their desired location online. Consider this. Your home is worth $500,000, but you list it for $575,000. When buyers are looking online, they filter to find homes within their price range and typically by $25,000 increments. The person looking for a $500,000 home will never see yours and if they do they will believe it is out of their reach, and when the buyers looking in the $575,000 range see your home and compare it to others in that range, they will get the impression it is not worth it, and there are better options.

Fewer people will see your home.

When your home is overpriced, the issue can be detected by buyers just by looking at your online listing and will pass on viewing it in person. The more showings you have, the more legitimate interest there is, and the more likely your home is to sell. Showings give potential buyers an opportunity to see the home first-hand giving them the opportunity to imagine themselves living there.

On the other hand, if you get lots of showings because your photos look better than reality but no offers you’ve wasted your best shot at getting the right buyer through your home and you there are no redo’s for first impressions. This leads us to our next point…

You are sending the “I’m an undesirable home” message to the public.

As people continue to look for a home and new buyers enter the market, they might see your home online, but by that time they will also see the “time on market”. The longer your home sits on the market, the less attractive it becomes psychologically to everyone. Nobody wants the home that nobody else wants. Once it has lost its appeal the damage is done. You’ll find yourself beginning to reduce your price and often end up at a price less than what the home could have sold for if it was priced right the first time.

In conjunction with price reductions, the longer your home sits on the market, the more expenses you incur. Consider mortgage payments, utility costs, lawn care maintenance, seller’s fees, and more while you are trying to move out.

Your buyers won’t be able to finance if it doesn’t appraise.

Perhaps you drop the price just enough to intrigue a buyer but still above market level. Maybe you’re lucky enough to hook a buyer. Then the appraisal comes back low. Now you either have to come down in price or lose the buyer and start over again, with 20-30 days more on market…

If you are considering selling your home and would like a complimentary analysis to determine the correct value of your home in this market connect with us to be paired with an experienced Windermere agent that can help you with your unique situation and avoid all the overpricing pitfalls.

What to Expect When Selling Your Home

Selling your home can be overwhelming and feel like a full-time job… which is why there are realtors! Good realtors make the process so much smoother and less intimidating. To keep your mind at ease and prepare you for what will happen throughout the sale of your home we are sharing 10 top tips to get you from listed to sold in no time!

Discover what to expect when selling your home

1. Select the right agent the 1st time

It is of the utmost importance that you pair with a full-time, knowledgeable agent who can best represent you through the process. This should be your number one priority. Studies show that homes listed with an agent sell for more than those listed without, and this is for good reason. Great agents dedicate their lives to keeping up with economic changes, are masters at negotiating and getting things done, and know all rules and regulations. This will pay off immensely in the long run if you trust their process. If you are unsure where to start, ask your friends who they trust and about their experience with them but don’t stop there. Interview at least two, preferably three brokers, and the differences should be immediately clear. If you still need help, Windermere has a full-time manager that will ask you pertinent questions about your needs, personality style, and specific goals to make the perfect real estate agent match. Windermere’s ultimate goal is not the sale of a home but to give you a real estate experience you want to share with others! When you are ready to pair with an agent connect with us and we will match you with the perfect broker.

2. Set your timeline

A timeline is valuable in that it will keep you organized throughout the entire selling process. Anticipate that your timeline might change depending on circumstances and your local housing market conditions. You may need to adjust a couple of times, but the purpose is to keep you on track toward your end goal. SOLD! Your timeline will help guide you there. Know what the average days on market are for your home and price range (click here to determine Whidbey Islands) then add an average of 30-45 on that to get an estimate of how long it will take to sell once you go live. Work with your agent to build your unique timeline.

3. Determine your home’s value

The SECRET to selling quickly is pricing your home right the first day it hits the market. Overpricing can create serious problems like not being seen by the right buyers, less traffic both in person and virtually, and worst of all becoming less attractive to buyers the longer it sits resulting in lower offers than if you priced it attractively, to begin with. Your agent will provide you with a (CMA) Comparative Market Analysis which compares your home to others in your local area that recently sold and/or are actively pending. This formulated analysis will assist you in properly determining the best price for your home. Discuss this with your agent. They will help walk you through the process even if you aren’t sure you’re ready to sell yet.

4. Identify issues & execute the plan

This is the time to tackle any unfinished projects and address needed repairs. Talk with your agent to see if a pre-sale home inspection would be advantageous for your unique situation. Begin by creating a list of repairs you can do versus those needing to be hired out. Your agent can help you determine which will be the best use of your time, offer the largest return on investment, and help you find vendors and hire out projects. If money is tight it may be in your best interest to apply to our Windermere Ready Program which gets you cash for fixing up your home to list. Ask your Windermere Agent about how to apply.

5. Put your best foot forward

First impressions go a long way! Start with curb appeal. Clean up your gardens, mow your lawns, clean out gutters, and add a pop of color to your flower beds. If you have any cracked or peeling paint, apply a fresh coat. Make sure to declutter the inside of your home. The best rule of thumb is to remove personal effects and present your home like a hotel in which the buyer could envision themselves living in the space. Talk to your agent about the possibility of having your home professionally staged.

6. Get your home seen

Your realtor will help maximize the exposure of your home. They can list with the MLS, will get your listing on all major sites like Zillow and Redfin, and will be listed on their Brokerage site in addition to their own. These are just a few of the many ways in which your listing can be seen. Be sure to discuss the option for virtual tours with your agent. When it’s time for in-person showings, we suggest that you not be present so that the potential buyers can freely walk the home with their agent, ask questions, and ultimately have the space to imagine it as their new home.

7. Reviewing offers & negotiating

If you price right, you might see more than one offer on your home because we are still in a strong Seller’s market. The offers may be at or above the asking price. When reviewing offers, you have three options: 1. Accept the offer, 2. Make a counteroffer, 3. Reject the offer. These should ALWAYS be made in writing, and you should always give the buyer a short time to respond. Whether you are selling or buying, you will likely find yourself in negotiations. It is important for you to discuss negotiation strategies with your agent ahead of time. At Windermere, we pride ourselves on negotiation tactics grounded in psychology and win-win strategies.

8. Budget for closing costs

Closing costs include things like title insurance, recording fees, government taxes, lender fees, broker commissions, and numerous other things. Be sure to discuss this with your agent ahead of time and throughout the transaction so you don’t feel blindsided at closing and are adequately prepared.

9. The inspection

It is common for offers to be contingent on a professional home inspection. Your agent can prepare you for what to expect from a home inspection. Typically a home inspector will look at things like the foundation, structure, roof, plumbing and electrical systems, floors, windows, doors, and signs for things like water or fire damage.

10. Closing

You finally made it, but before you can officially close there are a couple of things to do. Ask the buyer to release any contingencies, sign the title, and close escrow before releasing the keys. Your escrow agent will help you through this process. Talk with your agent about questions you have about legal documents and settlement costs.

If you are considering selling and would like to speak to an experienced Windermere Realtor for more specific information connect with us by clicking here.

The Benefits of Putting 20% Down on a House

If you read our, “How Long Does it Take to Save For a Down Payment?” article back in October, you know you don’t need a 20% downpayment to purchase a home because there are many alternative options available to you. However, while there are a plethora of options that you might qualify for, let’s look deeper into how putting 20% down could benefit you overall. You can find tried and true suggestions for saving up your downpayment here if you don’t have 20% saved up already. Keep in mind you can connect with us at any time to get personalized suggestions for what would work best for you in your unique situation.

In this article we are going to discuss how putting 20% down can help you get a lower interest rate, pay less overall, stand out in this competitive market, and avoid paying for PMI. Let’s get started.

Lower your interest rate:

A 20% down payment vs. a 3-5% down payment demonstrates to your lender that you are financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate will likely be.

Pay less overall:

The larger your down payment, the smaller your loan amount will be for your mortgage. If you are able to pay 20% of the cost of your new home at the start of the transaction, you will only pay interest on the remaining 80% of the cost of the home. If you put down 3.5 %, the additional 16.5% will be added to your loan and will accrue interest over time. This will end up costing you significantly more over the lifetime of your home loan.

Stand out in this competitive market:

In a market where many buyers are competing for the same home, sellers often like to see offers come in with 20% or larger down payments. Many buyers were hoping for the typical winter “slow-down” where they could see a less competitive market but that has proven not to be the case this year. Read more in our article, “Thinking the Housing Market is Going to Slow down this Winter? Think Again!” The seller in this current scenario gains the same confidence as the lender. You are seen as a stronger buyer with financing that is more likely to be approved. Therefore, there is a significantly higher chance that the deal will go through with a 20% downpayment.

Avoid paying for PMI:

You might be asking yourself, what is PMI? Freddie Mac explains,

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. . . . Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment.”

As mentioned earlier, if you put down less than 20% when buying a home, your lender will see your loan as having more risk than those who do put 20% down. PMI helps lenders recover their investment in you in the case that you are unable to pay your loan. However, this insurance is not required if you are able to put down 20% or more. In turn, this saves you from paying those extra fees.

Oftentimes, sellers looking to move to a larger or more expensive home are able to take the equity they earn from the sale of their house to put 20% down on their next home. The equity homeowners have today, creates an advantageous opportunity to put those savings toward a larger down payment on a new home.

If you are considering buying or selling or just want to talk about this in more detail, connect with us. We are here to help.

Why you should NOT wait to list your house right now

As the year comes to an end, we recognize a trend where homeowners are motivated to make the move and finally get into a home that complements their changing lifestyles. It is clear that homeowners have begun to understand the benefits of today’s sellers’ market. With record-breaking home price appreciation, growing equity, low inventory, and competitive mortgage rates it makes perfect sense as to why.

To support this, take a peek at recent data from realtor.com that demonstrates a significant share of homeowners that intend to list their homes this winter.

What That Means for Homeowners:

That means more homes are about to hit the market increasing supply to be more in line with demand than we have recently seen. This means there will be more options for buyers to choose from when looking for their homes.

According to George Ratiu, Manager of Economic Research at realtor.com:

“The pandemic has delayed plans for many Americans, and homeowners looking to move on to the next stage of life are no exception. Recent survey data suggests the majority of prospective sellers are actively preparing to enter the market this winter.”

If you are thinking about waiting till the spring to sell your house, keep in mind that your neighbors might be one step ahead of you and sell this winter. If you want to stand out from the crowd, this holiday season is the best time to make sure your house is available for buyers. Here’s why.

Sellers Are Still Firmly in the Driver’s Seat:

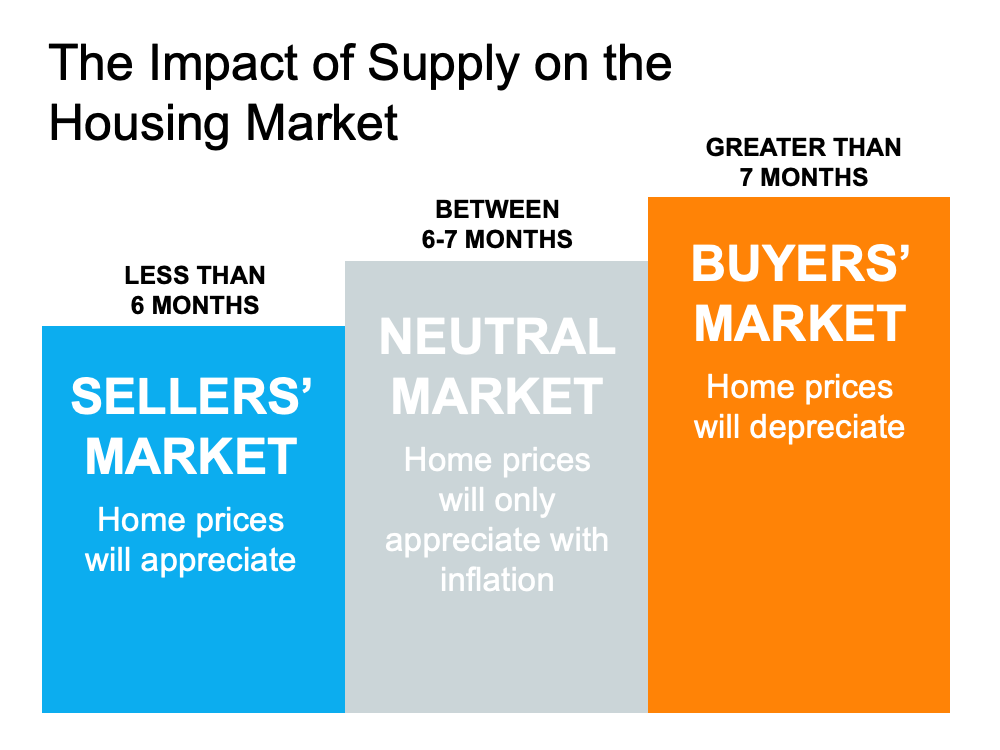

Historically, a 6-month supply of homes for sale is needed for a normal or neutral market. That level ensures there are enough homes available for active buyers (see graph below): The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows the inventory of houses for sale sits at a 2.4-month supply. This is well below the 6-7 months supply needed for a neutral market.

The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows the inventory of houses for sale sits at a 2.4-month supply. This is well below the 6-7 months supply needed for a neutral market.

What Does That Mean for You?

When the supply of homes for sale is as low as it is today, it is more difficult for buyers to find homes to purchase. This drives up competition among buyers, who then submit increasingly competitive offers to win out against others in the home search process. As this happens, prices rise and your leverage as a seller rises too, putting you in the best position to negotiate a contract that meets your ideal terms.

The low housing supply we are currently facing will not be solved overnight. Sellers this season should act quickly to maximize their potential. The data demonstrates that, with more prospective sellers planning to list their homes this winter, selling sooner rather than later helps your house rise to the top of a holiday buyer’s wish list so you can close the best possible deal.

Bottom Line:

Listing your home over the next few weeks gives you the best chance to be in front of buyers competing for homes this holiday season. Let’s connect today to discuss how you can benefit from today’s sellers’ market. Email us here.