Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Benefits of Putting 20% Down on a House

If you read our, “How Long Does it Take to Save For a Down Payment?” article back in October, you know you don’t need a 20% downpayment to purchase a home because there are many alternative options available to you. However, while there are a plethora of options that you might qualify for, let’s look deeper into how putting 20% down could benefit you overall. You can find tried and true suggestions for saving up your downpayment here if you don’t have 20% saved up already. Keep in mind you can connect with us at any time to get personalized suggestions for what would work best for you in your unique situation.

In this article we are going to discuss how putting 20% down can help you get a lower interest rate, pay less overall, stand out in this competitive market, and avoid paying for PMI. Let’s get started.

Lower your interest rate:

A 20% down payment vs. a 3-5% down payment demonstrates to your lender that you are financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate will likely be.

Pay less overall:

The larger your down payment, the smaller your loan amount will be for your mortgage. If you are able to pay 20% of the cost of your new home at the start of the transaction, you will only pay interest on the remaining 80% of the cost of the home. If you put down 3.5 %, the additional 16.5% will be added to your loan and will accrue interest over time. This will end up costing you significantly more over the lifetime of your home loan.

Stand out in this competitive market:

In a market where many buyers are competing for the same home, sellers often like to see offers come in with 20% or larger down payments. Many buyers were hoping for the typical winter “slow-down” where they could see a less competitive market but that has proven not to be the case this year. Read more in our article, “Thinking the Housing Market is Going to Slow down this Winter? Think Again!” The seller in this current scenario gains the same confidence as the lender. You are seen as a stronger buyer with financing that is more likely to be approved. Therefore, there is a significantly higher chance that the deal will go through with a 20% downpayment.

Avoid paying for PMI:

You might be asking yourself, what is PMI? Freddie Mac explains,

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. . . . Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment.”

As mentioned earlier, if you put down less than 20% when buying a home, your lender will see your loan as having more risk than those who do put 20% down. PMI helps lenders recover their investment in you in the case that you are unable to pay your loan. However, this insurance is not required if you are able to put down 20% or more. In turn, this saves you from paying those extra fees.

Oftentimes, sellers looking to move to a larger or more expensive home are able to take the equity they earn from the sale of their house to put 20% down on their next home. The equity homeowners have today, creates an advantageous opportunity to put those savings toward a larger down payment on a new home.

If you are considering buying or selling or just want to talk about this in more detail, connect with us. We are here to help.

The Search for Equestrian Property

Buying property suitable for horses is no small task. It is certainly not the typical home buying experience. There is so much to consider from what kind of property best meets the needs of your horses to what kind of home will best meet your wants and needs. Speaking from experience, the horses’ needs are typically the priority.

Working with an experienced Equestrian Advisor/Realtor will also help ensure your home search and purchase go as smoothly as possible. You can find one here.

The Property has Acreage: Is it Suitable for Horses?

Any Equestrian Advisor/Realtor will be the first to tell you that, just because a property has plentiful acreage does not mean it will be a suitable property for your horses. The best property will be flat to gently sloped with good drainage, open areas with grass for grazing, with few trees, and wet areas. Horses weigh 1000 to 1500 pounds on average, which puts a lot of weight on the ground. Therefore, horses can do a lot of damage in a short amount of time.

The priority is finding an Equestrian Property with useable land – meaning not acres of unusable gullies, steep edges, or too many bodies of water. More land doesn’t necessarily mean it is better, the useability is the priority.

Amenities:

Housing horses and livestock on your property can be done with ease with a few convenient amenities. It is important to consider these amenities as they add value to the Equestrian Property:

- Barn – Does it have an adequate number of stalls for your needs and the right size for your type of horse? Horse stalls can measure from 10 x 10 to 12 x 12 or even larger. Does it have the capability to increase the size of the stall to make foaling stalls? Are the stalls matted? Are there runouts (sacrifice paddocks) off the stalls?

- Hay Storage – What style is the barn? If it is a Monitor style barn, does it have a hayloft? How much hay can be stored in the hayloft? If there is no hayloft, is there adequate storage for hay elsewhere?

- Tack Room – Does the barn have a tack room? If so, is it insulated? It is important to be able to store tack, brushes, and other items in the tack room without them getting damp and moldy.

- Tack Area and/or Wash Bay – While one can do without this amenity it sure is a bonus to have it.

- Quality and Safe Fencing – Fencing can be quite costly (please watch for our future blog on fencing). It adds a lot of value to an Equestrian Property to have good quality and safe fencing. Equally important is how well it is laid out on the property. Is the property fenced and cross-fenced?

- Arena (Indoor and/or Outdoor) or Training Round Pen with good footing – It is a huge bonus to find a property with an arena, especially an indoor arena. Indoor arenas are getting increasingly more difficult to get approval to build and depending on the size can cost well over $100,000 to build. Outdoor arenas are great but have their challenges. It becomes difficult to manage the footing due to weather. Footing in the arena is something to really consider. Each discipline has its own preferences for footing type and depth. But any equestrian will agree that poor footing can cost you a lot – cause lameness in your horses resulting in expensive vet bills and not to mention the time to rehabilitate the horse from injury.

- Water source and location of water on the property. Are there ample spigots to the pastures/paddocks and arena?

- Electricity – Does the barn have electricity running to it?

Your Routine:

Transitioning to an Equestrian Lifestyle is a big adjustment. Make sure you are taking your daily routine into consideration when looking at properties. Consider the layout of the Equestrian Property. Does it seem that your daily routine will be seamless i.e., bringing horses in and out from pasture/paddocks to the barn? Are there turnouts off the barn that make it easier on your daily routine? Where is the manure kept? Ultimately, as an Equestrian, you want to be able to leave your property and know that your horses will be safe and sound while you are away.

Barn(s) and Outbuildings Should be Inspected Too:

You have found your Equestrian Property. It will cost you extra, but it is important to have your inspector inspect the Barn(s) as well as the Outbuildings. Your horses are part of your family, and you want to make sure that they will be safe in their surroundings. It is important to have a professional evaluate the Barn and Outbuildings for structural issues, electrical issues, or other potential problems.

Zoning Regulations:

Do not assume that the property is an approved horse property just because the owners or prior owners have had horses on the property in the past. Part of the Inspection process will be to do a little research with local city, county, and/or HOA regulations for agriculture and livestock. Do not let this lack of research cut into your dreams of owning an Equestrian Property.

Let us help you make your dreams of owning an Equestrian Property a reality:

To be honest this is all just the tip of the iceberg when searching for an Equestrian Property. It helps to have someone working for you that has done this before. Let’s get you connected. It would be an honor to help you make your dreams a reality.

Things to do Today to make you a Homeowner Tomorrow

As the gap between the cost of rent and the cost of a mortgage continues to close, we see an increasing number of renters interested in buying. But how can renters make the transition to owners?

The purpose of this article is to help renters implement three critical changes today to help them successfully purchase a home tomorrow. If implemented correctly, these changes will help renters overcome the feeling of never being able to purchase a home.

Start by talking with a local lender

Do your research. Find a trusted lender in the location you are planning to purchase your home. Why is it important to use a local lender? Each housing market is different depending on location. Despite the similarities in names, what might be happening in San Francisco may not be happening in San Antonio. It is important to talk to a lender that is not only familiar with but understands the current local market and can explain to you what it takes to become a first-time homeowner. Check out our full article here. Your trusted advisor can then look at your specific financial situation and make suggestions to help you navigate the local market, meet your specific needs, and discuss your available options. This conversation can help you build your timeline for when it is right for you to purchase. Having the right team of real estate and lending professionals on your side can help tremendously when planning for your first home. Together they can help you determine your goals, what you can afford, and help you get pre-approved when you are ready. Need help finding a lender? Click here.

Reduce your debt and build your credit

Your first step should be knowing your credit score and what it means. Check out this article here for more information on credit scores. According to the HUD, the average credit score of first-time homebuyers is 716. There are many online tools that can help you determine your credit score. If you don’t already know yours it would be advantageous for you to find out.

If you determine that your score is below 716, don’t freak out.

First, 716 is just an average which means that there are homeowners with credit scores both above and below that number. Knowing your score gives you a snapshot of how you are doing financially and helps you know how to adjust accordingly to reach your goals.

Second, there are numerous ways to increase your credit score BEFORE you apply for your home loan.

- HUD’s number one recommendation is to reduce your debt as much as possible. Start by reducing your current spending. This will not only help you have less debt, but it will also help you have more money to pay down your current debts. Start small, perhaps purchasing one less coffee a week or choosing water instead of the soda or martini. These small sacrifices now will add up to big wins later. We recommend TrueBill as an app that can help find hidden savings by canceling subscriptions you don’t use anymore or negotiating your existing subscriptions down. It can also help you develop and stick to a budget!

- Pay all your bills on time. Set up auto payments to avoid late payments.

- Use your credit card responsibly.

When you have your debt in a manageable place…

Start saving

It might already feel like you are barely making it. But it has been proven that setting aside even small amounts can make it possible for you to save for a down payment on a home over time. Having funds in savings is also taken into consideration when getting pre-approved for a home loan (See why getting pre-approved is imperative). You don’t always need a large down payment when buying a home but you will need a good house fund saved up for ongoing maintenance and repairs.

Many experts suggest using a hidden savings or a “sinking fund” when saving for your down payment. This is an “out of sight out of mind” savings account. Once money goes in you don’t take it back out till you are ready. Make sure you keep it separate from your emergency fund or your short-term savings for expenses. Set small attainable goals that make you feel accomplished rather than the large goal that might feel daunting and overwhelm you. Are you ready for the challenge?

See how long it takes the average person earning a medium-income in America to save for a down payment here.

In conclusion, get some professionals on your team by talking with a lender (ask your trusted Windermere Broker for recommendations) if you don't have an agent contact us here and we will get you connected, build credit, and start saving!

How Long Does it Take to Save For a Down Payment?

Saving enough money for a down payment on your first home can be one of the biggest obstacles to homeownership. Depending on your circumstance you might need anywhere from 3% – 20%. Speaking with a reputable local lender will help you find out exactly what your percentage will be.

But how long should it take, you ask!?

Follow along as we estimate the amount of time it takes a person earning a median income and paying a median rent to save up for a down payment on a median-priced home.

To accomplish this task we use the concept that homeowners should pay no more than 28% of their total monthly income on housing expenses. We use this information in combination with data from the U.S. Department of Housing, Urban Development (HUD), and Apartment List to determine our estimation.

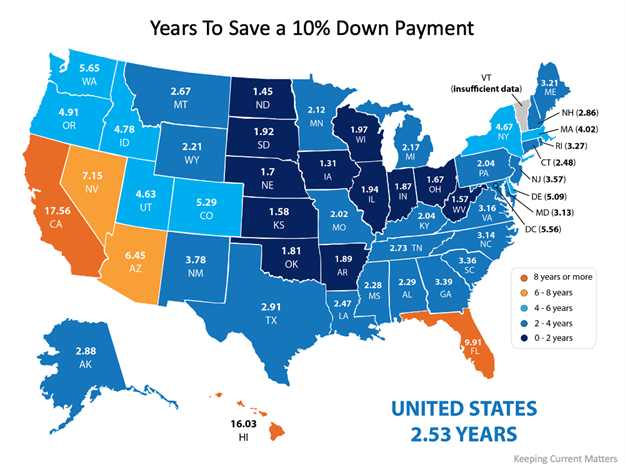

According to the data pulled, the national average for the time it would take to save for a 10% down payment is roughly two and a half years (2.53). Looking at the diagram below you can also see that those living in Iowa can save for a down payment in as little as 1.31 years while those in California could take 17.56 years. The map below can help you determine the amount of time (in years) it can take for you to save in your state:

What if you only need to have a 3% down payment?

It is a common misconception that you need to have a 20% down payment to buy a home.

The reality is there are reasonable alternative options out there. First-time home buyers have an advantage with a plethora of down payment assistance programs available to them. You just have to find the right lender and ask. Need help finding a lender? Ask us to connect you with one here.

What if you qualify to take advantage of one of the 3% down payment programs?

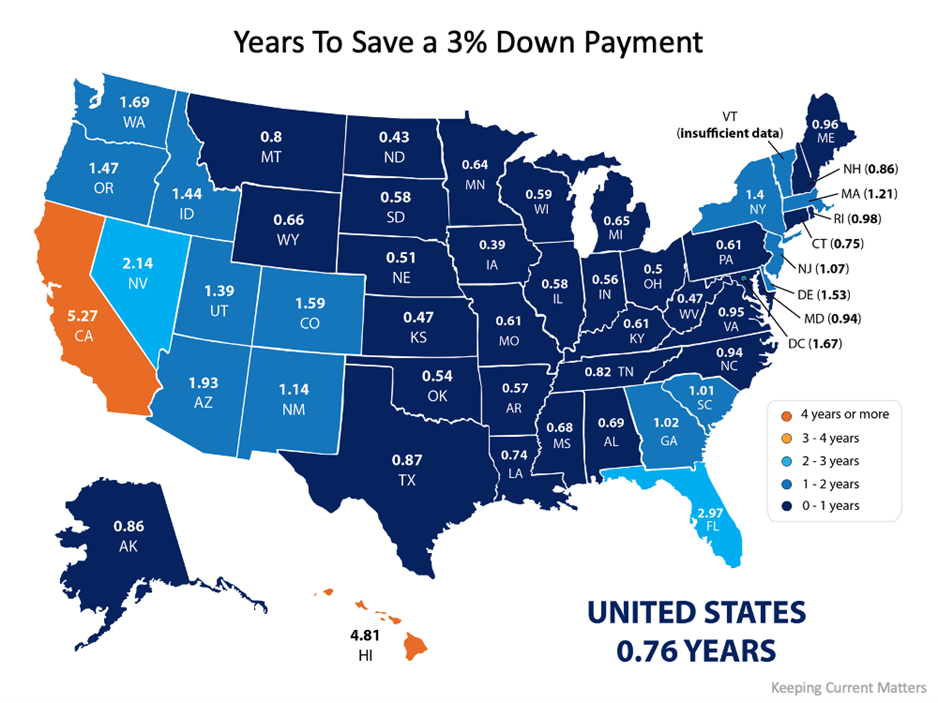

If you qualify for a 3% down payment program, then you only have to come up with 3% of the total cost of the home at closing instead of ten or the typical 20% we have seen required in the past. Saving for a 3% down payment might not take you very long. In fact, it could take less than a year in most states, as shown in this map here:

At the end of the day

Wherever you are in the process of saving for a down payment, you may be closer to your dream home than you think. Connect with us to explore the options available to you in our area and how they support your plans for buying a home.

4 Online Resources That will Blow Your Mind!

…and help when buying vacant land on Whidbey Island.

ICGeo

This is a sophisticated GIS mapping tool for Island County that can show layers and layers of geographically specific data overlaid on a map. Just turn on the layers of data you are interested in and search till your heart is content!

Island County Public Portal

Use this tool to look up a parcel number or a street address to determine if there are any site registrations, septic permits, or septic as-builts done for the parcel. It will also disclose any permits a property has recently applied for and its status.

Groundwater Spatial Analysis Report

This tool analyzes the potential groundwater quality at any given spot on the island by grabbing the data on wells within 1/8 mile of the point you choose on the map (or the nearest 40 wells). It automatically generates a phenomenal report. Just submit the application and the report is emailed to you almost immediately. This document will offer you more detailed information on what you get in the report

Washington Coastal Atlas Map

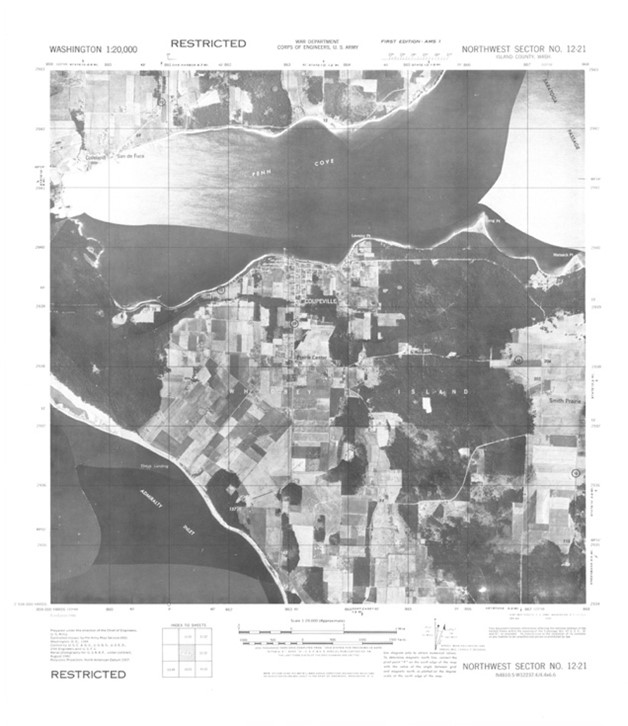

With the Shoreline Photo Viewer, you can compare what has happened to any stretch of shoreline over the last 50 years through photography! This tool uses 5 photo sessions capturing images of our shoreline all the way back to 1970. Even if you are not currently buying waterfront land this is a fun tool to compare what has happened to any section of our shoreline. There are even aerial photos from the 1940s. Check out the image below taken before Rolling Hills or Penn Cove Park were developed.

To find more amazing tools at your disposal or to get help using these tools to find specific information you can call us, and we will connect you with one of our knowledgeable Windermere brokers. You don’t have to be actively selling or buying a home! We just love to help! Contact us here.

Set Yourself up for Success by Doing These 7 Things When Buying Your First Home

Buying your first home can be easy when you are adequately prepared and you have a good agent on your side. But where to start and what actions are most important? We will get you pointed in the right direction. Let’s get started!

-

Know your credit score.

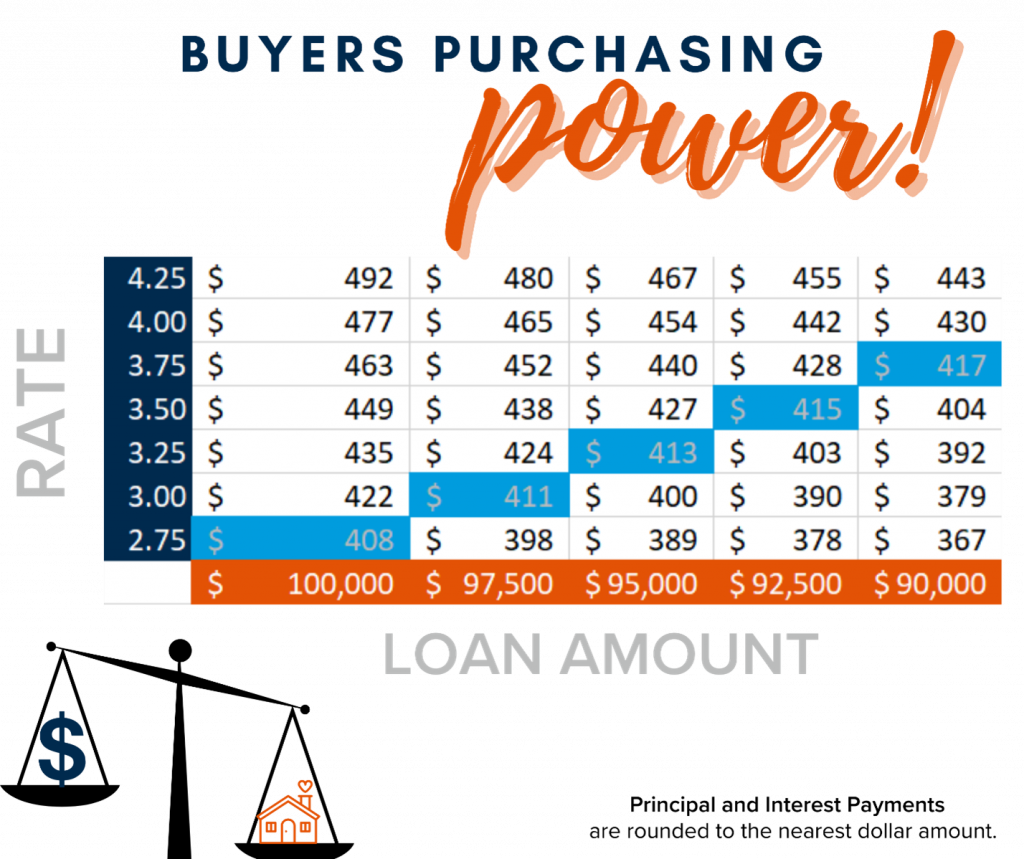

Many first-time homebuyers fail to recognize that one of the most important factors in getting approved for a mortgage is their credit score. The health of the score determines not only the interest rate but also whether they will be approved for a mortgage in the first place. Some people wonder why the interest rate really matters. The truth is that the slightest difference in rate can mean big money over 30 years! As the chart below demonstrates, a lower interest rate helps buyers afford a higher-priced house and still pay less monthly. Check out this article to learn more about Credit score rankings and what they mean.

-

Set a clear budget and stick with it.

Another big mistake first-time homebuyers make is not budgeting realistically and then finding out they cannot really afford the house they chose. A great way to get an idea of how much you should realistically spend on a mortgage is to determine your debt-to-income ratio. This number can be calculated by adding all your monthly debt payments (mortgage, credit card bill, car payment, etc.) together and then dividing by the gross monthly income. A conservative percentage of your income spent paying down debt would be 20-25%, a medium would be 25-30%, and a high would be 30-38% (or higher when using gross income vs. net).

-

Remember there are other fees other than the mortgage payment.

Homeownership comes with fees and other bills that you may not have as a renter. In addition to principal and interest on the mortgage payment, there will be real estate taxes and homeowner’s insurance. Check to see if the home is part of a homeowner’s association as there may be annual or monthly dues for that (a great agent will let you know about this). These fees typically show up as part of the mortgage payment. However, what is often forgotten or inaccurately calculated is the utility bills like water, sewage (or septic inspections/pumping), garbage, and energy bills. Furthermore, unlike renting if a pipe breaks or roof leaks there is no maintenance man that just shows up to repair it. Remember to budget for the maintenance of the home. This includes mowing the lawn… do you have a lawnmower yet?

-

Leave a cushion.

As discussed, buying a home has a lot of upfront costs. A bank account that seemingly had a plethora of cash can quickly be drained after the down payment, closing costs, moving expenses, and furnishing a new home. Having a healthy emergency fund is so critical as a homeowner.

Check out this helpful article by Dave Ramsey.

-

Once steps 1-3 are completed get pre-approved.

Don’t just meet with any lender, be sure to find a highly reputable local lender that the top listing brokers recommend (this will give you a competitive advantage). Not only does the pre-approval give buyers a realistic idea of how much they can borrow, but it can also be the defining factor of whether or not they get the home. Let us explain. A pre-approval speeds up the process and demonstrates the person is a serious buyer, not just a lookie-loo. When it comes down to multiple offer situations, as we see so frequently now, it is critical to have the most well-presented offer. Showing the seller that you are not only serious but that you have been pre-approved for the funds needed to buy with a lender they respect sends a strong message that you are the one the seller should choose! Check out our local lenders here.

-

Ask questions about your options!

Not everyone’s situation is the same. Similarly, loans are uniquely created to fit individual needs. Historically, it has been thought that buyers need to come to the table with at least a 25% down payment. Today that is just not true. While it is always good to have money for your mortgage down payment, there can be alternative options if you don’t. VA mortgages can be secured for 0% down and conventional mortgages for as little as 3%. Check out these different mortgage types meant to uniquely fit your life.

-

Hold off on any spending spree and do not take out a line of credit.

Remember that “debt-to-income ratio” mentioned above? Your mortgage approval is linked heavily to this number. This is not the time to go out and buy a new sportscar, purchases new appliances, and or upgrade your electronics. Borrowing money after getting pre-approved increases the debt-to-income ratio, and this will be re-checked just prior to the loan being approved. Applying for a new loan or credit card will also likely decrease your credit score. If either of these things happen prior to closing it could mean losing the mortgage and the interest rate you locked in. So, hold off on spending or even giving out your social security number to anyone!

We hope this helps point you in the right direction. We would love to be your guide as you prepare and navigate the path to homeownership! Call us today and we can connect you with an expert Buyers Broker! 360.675.5953.

If you enjoyed this you might also like:

5 Most Affordable Neighborhoods Near Oak Harbor & NAS Whidbey

5 Things Every Septic Owner Needs

A Drain Snake

Don’t kill your system with Drano! Hair clogs happen. Instead of pouring caustic Drano into your plumbing (which can actually cause damage to pipes and will kill your septic system) try this super cheap (less than $2 each) and easy drain snake that works in seconds. This tool coupled with prevention (see #2 below) will keep you from having to resort to expensive and dangerous remedies.

A Drain Cover

There are hundreds of different types of drain covers. We have tried several to reduce the guess work for you and discovered that we like this flat and wide version best. You can order it here. Honestly, regardless of which kind you purchase your septic will thank you as long as it keeps hair and other large particles from swirling down your drains to prevent it from clogging and will save your septic.

The Right Toilet Paper

Most people are too dignified to talk about things related to the potty but as a septic system owner you need to know that there is a right and a wrong kind of toilet paper if you want to keep your system in excellent condition and prevent clogging. If you put a piece of your TP in a glass of water, stir it up a bit and let it sit for a few minutes it should dissolve pretty quickly into tiny pieces no larger than a nickel. This is called the TP test. If it stays intact in larger pieces your septic system is going to have a real problem breaking it down and the chances of you clogging your toilet are MUCH higher. Check out the results from a test The Art of Doing Stuff did here.

A Pumice Stone

With hard water being the rule and not the exception on Whidbey Island there is a constant battle to keep our toilet bowls and sinks free from the dreaded hard water rings. Using harsh chemicals to try and remove them can work but at the cost of damaging the function and life of your septic system. The solution? A simple and cheap pumice stone! A wet pumice stone won’t scratch porcelain but it will easily and effectively remove hard water build up just by rubbing it back and forth across the stain. Try it and let us know what you think!

A Good Septic Inspector

Because you now own your very own mini sewage treatment machine you will need to maintain it. Finding a great septic inspector and getting on a regular inspection rotation is as easy as picking up the phone and calling or texting your Windermere Broker. At Windermere we pride ourselves on always having the inside knowledge about and great relationships with vendors our clients will need. Septic inspectors are #1 on that list! Many of them have a program you can join that puts you on a regular inspection rotation so you don’t have to think about it every year (or 3 years depending on your system). If you don’t have your very own Windermere Broker you are missing out! Visit our website to find your match today

If you liked this you might also like:

Blonde Lawns Whidbey Island Utility Costs

Buying Vacant Land on Whidbey Island

If you have always dreamed of building your own home, choosing your own layout, selecting dream finishes, and want all your desires in a home met then you will be looking for vacant land. This is a completely different world than buying a preexisting home where there is complete certainty when it comes to electricity, water, sewage, and condition. Uncertainty is not comfortable for everyone so let’s make sure you feel prepared and empowered.

First and foremost, if you ask anyone who has built their own home, they will tell you that even if you build a home from scratch you will not end up with a 100% perfect house. There are always compromises and unforeseen issues with layout, etc. Remember, vacant land is scarce and becoming scarcer, so if you find the perfect property with an imperfect house, perhaps you can consider a major remodel.

When buying vacant land, it is all about the level of certainty a parcel can provide you. A parcel that already has a water source, septic system, access/driveway, building site laid out, and electrical nearby is going to be extremely rare. Such a parcel will cost more because of the time and expenses already invested by the seller. There is also inherent value in the confidence you as a buyer can have that you will not run into complications that may make the land unsuitable for development.

Below are our TOP 5 recommendations when considering buying vacant land:

Find a vacant land purchasing specialist.

Complex is the word that comes to mind when thinking about vacant land purchases. Having a trusted guide who loves the complexity that comes with purchasing land is something you really want. Many brokers groan when they think about helping buyers with vacant land but there are a special few who just dig it! Find them! It will make all the difference. If you need a recommendation just call (360) 675-5953 and ask for a recommendation on a vacant land specialist from the manager.

Know your corners.

In the best-case scenario, there has been a survey done and the corners are clearly marked with modern official survey markers however, this is rare. You may need to negotiate to have this done by the Seller. There are other signs that can give an idea of where property lines fall though. One of the coolest technologies that most agents have nowadays is an app that uses geo-spatial technology to locate your position on a map in relation to property lines. An old-fashioned surveyor’s tape measure can help as well if you have a marker of some sort to start from. Fence lines, survey tape marking trees or branches, driveways, and other identifiers can give clues. Nothing beats a proper survey though and you are going to want that when it comes time to build.

Get as certain as possible on the big 5.

Water, sewage, electricity, access, and building envelope. These are the big 5 mysteries when you first look at a raw and overgrown piece of land. The more that these 5 things have been figured out and addressed by the Seller, the more valuable the property is. You are buying risk when these 5 are unknown. You cannot avoid risk completely but figuring out as much as you can about these 5 will help you move forward more confidently.

Work with a local builder.

Get the local builder to the lot sooner than later. Reputable builders on Whidbey will be able to help you through the feasibility process, have a great instinct for what is possible, contacts to get specialists out to the property, and experience working with Island County’s Building department. Here are 5 builders we recommend in no particular order…

Know your critical areas.

Shorelines, native American artifacts, endangered animals and plants, steep slopes and bluffs, wetlands, and streams will affect the property in big ways. There are large set-back requirements for structures, wells, and septic systems around critical areas. You may get into a situation where you do not have much of a choice about where you can position your building site. These unknowns must be understood before you decide to close on the lot. Your Realtor can help you navigate this maze.

Each property is unique, and we could share a lot more with you on the topic of buying vacant land on Whidbey, but the truth is that the best thing you can do is find yourself an excellent guide who will help you assess what it is you are really looking for and how to narrow down the search. Good luck and do not forget your muck boots!

PHOTOS BY: Kelsey Kurtis