Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Perfect Time For You

The housing market is continuing to shift as inventory levels rise and buyers gain more options. If your home search was put on pause these past few years, you’re not alone. Luckily for you, there are options. Today’s current market might be the perfect time for you to resume looking. Let us explain why.

Currently we are seeing an increase in homes for buyers to choose from. In addition to the increase in inventory many buyers are noticing that prices have begun to level off in many areas. Pair increased inventory and leveling prices with mortgage rates that have begun to ease, and today’s market is currently the one many have been waiting for.

Continue reading for the breakdown.

Increased Inventory

With more homes coming onto the market and months of inventory increasing, we’re moving away from the highly competitive seller’s market we’ve experienced over the past several years. Buyers now have more choices, additional time to make decisions, greater negotiating power, and less competition with other buyers. Allowing buyers a more enjoyable purchasing experience and the ability to truly find their perfect home. While well-priced homes are still selling, the increase in available inventory is creating a more balanced market. A balanced market offers opportunities for both buyers and sellers.

Therefore, if you are selling, now more than ever it is of the utmost importance to have a trusted, professional realtor on your side. Your realtor can help position your property appropriately, be more strategic with pricing, and increase your homes presentation to stand out to get your home seen by potential buyers. Need a trusted realtor? Connect with us.

The Big Picture

The United States is experiencing more homes on the market compared to the same time last year. We know what you’re thinking. “Not every market is the same, and how does it compare to pre-covid numbers?”

In the South and the West inventory has fully recovered and in some places even surpassed pre-pandemic levels. However, supply remains tighter in much of the Northeast and Midwest where inventory is still below the historical normal. It is important to always discuss with your Realtor what the market looks like in your market.

More Choices Everywhere

Even with not every area fully recovered it is still a win for everyone. When you look at the bigger picture, inventory is up in every region. That means more choices everywhere, even though some areas have more homes for sale than others. With fewer buyers in the market and more homes for sale, sellers are willing to negotiate to get a deal done.

What’s happening in your area might look different than the national or regional trend. It’s important to work with a local Realtor that can help you understand your market and positioning. If you previously paused your home search this could be the time to take another look.

Maybe you’re still not ready. Connecting with your trusted Realtor now can help you prepare your budget, narrow your search, and make sure you fill prepped when the right home does show up on the market.

2026 Homestay Program

There’s something special about real estate bringing people together from completely different corners of the world. We recently got the perfect reminder of that! One of our brokers, Karen Cox, had the absolute pleasure of hosting Undraa. Undraa is a talented realtor who visited us all the way from Mongolia as a part of the Washington REALTORS ® 2026 Homestay Program. As part of their ongoing global initiatives, this program offers members of the Mongolian ambassador association a unique opportunity to experience the day-to-day life of REALTORS® in the U.S. The experience also provides U.S. REALTORS® valuable insight into the impact and importance of Washington REALTORS®’ global partnerships.

A True Cultural Exchange

From the moment Undraa arrived, it felt like a true cultural exchange rooted in shared passion, curiosity, and a love for helping people find the beautiful sanctuary they will call home.

Karen Cox said:

“Having gone to Mongolia last year, I was excited to host a Mongolian agent. I never met Undraa on my trip to Mongolia with Washington Realtors®, but we discovered we were in some of the same photos from the Realtor’s Voice Forum I attended in Mongolia.”

The Experiences

One of the best experiences was when Undraa offered to cook us a Mongolian meal. She made us Khuushuur (fried dumplings) and Buuz (steamed dumplings). They were delicious! She explained their whole family gets together on holidays and makes these. Like us cooking for Thanksgiving, but on a larger scale because they often have all the extended family there too.”

During her time here, Undraa and Karen explored the beauty of Whidbey Island together, touring a variety of listings and soaking in everything that makes this place so unique. From waterfront views to quiet countryside properties, it was a chance to not only showcase our local market, but to see it through a fresh set of eyes.

The Connection

We loved having the chance to host lunch to welcome her to Whidbey Island! Brokers from both our Coupeville and Oak Harbor offices convened to connect with each other and with Undraa to share meaningful conversations and listen to her experiences. After lunch, we got the chance to see a presentation from Undraa on the real estate processes in Mongolia, insights about how she serves her clients, and the differences between real estate in Mongolia versus here! From differences in property ownership to the pace and structure of transactions, it was fascinating to compare and realize just how global (and yet personal) this industry truly is.

But beyond the business side, what made this visit unforgettable were the moments in between.

Undraa spoiled us with thoughtful gifts from Mongolia, each one carrying a piece of her home and culture. And then, she went a step further—preparing us a traditional Mongolian dinner that brought everyone together around the table. It wasn’t just delicious (though it absolutely was); it was meaningful. Food has a way of connecting people, and that evening was more than just a meal; it was the blossoming of a beautiful new friendship.

The 2026 Homestay Program Success Story

Experiences like this remind us that real estate isn’t just about properties—it’s about people, stories, and connections that stretch far beyond borders.

We miss her already.

Thank you, Undraa, for sharing your knowledge, your culture, and your kindness with us. Enjoy the rest of your time in the U.S.! We’ll be cheering you on from Whidbey Island!

Real Estate Ranking in Puget Sound

The Puget Sound Business Journal released real estate rankings that truly made us proud to be part of Windermere (check them out here). Windermere has been a long standing leader of market leadership in the Puget Sound area and this report confirms that has not changed. The report claims Windermere Puget Sound did $21.32 billion in residential sales volume in 2024, surpassing the closest competitor by nearly a threefold. The report demonstrates how Windermere Real Estate continues to assert its position as the foremost residential real estate firm in the Puget Sound region.

The history:

The Puget Sound Business Journal inaugurated its list of top residential real estate companies in 1986. Windermere has maintained the No. 1 ranking every single year. This nearly four-decade tenure spotlights not only Windermere’s market share but its sustained organizational resilience, strategic adaptability, and strong community presence. We are proud to be a part of the success.

Factor of Success:

Several factors contribute to Windermere’s enduring success. First, its expansive network across the Pacific Northwest supports unparalleled market coverage and client reach. Second, the emphasis on agent education, technological integration, and customer-centered service has strengthened its professional reputation and operational efficiency. Finally, Windermere’s deep-rooted commitment to community engagement. The Windermere Foundation, funded in part by a portion of every home sold sets Windermere apart as both a market leader and a socially responsible organization. As Windermere offices and agents in the Puget Sound, we couldn’t be more proud.

Here is a snip-it into what our Oak Harbor and Coupeville offices have been doing in our communities recently:

What it all means:

Windermere’s continued ability to maintain leadership at such scale suggests a robust alignment between regional market demands and Windermere’s business model. Housing markets across the Puget Sound area evolve in response to demographic shifts, economic pressures, and ongoing development patterns. Windermere’s legacy of leadership positions it uniquely to shape the future trajectory of real estate services in the region.

In sum, Windermere’s top ranking is not merely a reflection of annual sales. Windermere’s top ranking is a testament to nearly forty years of consistent excellence, strategic foresight, and unwavering commitment to all of the communities served. We are grateful for your continued trust in our services and look forward to continuing to serve you for years to come.

If you are looking to making a move in your future please reach out. We would love to help you. If you wish to have a copy of this document mailed or emailed to you please email us at whidbeycommunications@windermere.com.

Fall Garden & Yard Prep

Fall Garden & Yard Prep: Setting Your Home Up for Success

Early fall warm weather days often tempt us to keep our gardens going just a little longer, but late September through October is the prime time to prepare your yard for the colder months ahead. Think of it as “winterizing” your home’s curb appeal—a little work now means a smoother, fresher start come spring.

Just like a home needs the right foundation to thrive, your garden and landscape need a strong send-off before winter arrives. Here are a few smart (and surprisingly simple) steps every homeowner should take:

1. Say Goodbye to Summer Veggies

As much as we want those last tomatoes to ripen on the vine, it’s time to let go. Pull spent veggies like tomatoes, peppers, and cucumbers, and add them to your compost. Still have green tomatoes? Don’t toss them! You can ripen them indoors by placing them in a paper bag or box.

2. Care for Perennials

Healthy perennials can be left standing; they’ll catch snow and add some winter charm. However, if there are any plants that show disease, they should be removed now to prevent problems next year.

3. Hydrate Before Hibernate

Trees, shrubs, perennials, and even lawns benefit from a good soak before the freeze. A well-watered root system means a healthier comeback in spring.

4. Empty Containers

Ceramic, terra cotta, and clay pots don’t do well in freezing temps. Clean, dry, and store them to prevent cracking.

5. Clean & Store Tools

Wash your garden tools, sharpen blades, and lightly oil metal surfaces to keep rust away. Your future self will thank you when spring planting rolls around. If you accidently left one out and it now has some rust, esteemed Minnesota gardener and writer Mary Lahr Schier has a tip for you. Discover her secret in her article by clicking here.

6. Manage the Leaves

A light layer of chopped leaves can be good mulch, but too many leaves left on your lawn may cause snow mold and damage your grass. Rake or mulch as needed. Keep aside some leaves to use as mulch after the soil freezes.

Why It Matters for Homeowners

Not only does fall yard prep make spring easier, but it also protects your landscaping investment, boosts curb appeal, and helps your home shine year-round. Whether you are thinking of selling next season or just want to love the home you are in, small steps now add long-term value.

So, grab your rake, pull on your cozy sweater, and show your home a little autumn TLC—it’ll pay off in more ways than one!

If you are thinking about selling next season now is the best time to connect with a realtor to help guide you every step of the way, feel free to connect with us. Find our contact details here.

Minimizing the Stress of Selling Your Home

Minimizing the Stress of Selling Your Home: Navigating the Emotions and the Process

Selling your home is more than just a transaction; it’s the closing of one chapter and the beginning of another. For many homeowners, the process is not only physically demanding but also emotionally overwhelming. After all, you are not parting with just a property, you may be leaving behind a space filled with memories, milestones, and meaningful moments.

While the process of selling a home can be daunting, there are practical steps you can take to minimize the stress and make the experience smoother. Follow along for an approach to selling your home with confidence and clarity, while honoring the memories you have made along the way.

Acknowledge the Emotional Side of Selling

It’s perfectly natural to feel sentimental when preparing to sell your home. Over the years, you’ve celebrated birthdays, holidays, and milestones within those walls. Instead of pushing those feelings aside, acknowledge them. Take a walk through your home and reflect on the positive memories you’ve created.

If it helps, capture a few meaningful photos of your favorite spots in the house or yard. This can give you a sense of closure while also preserving the memories you’ve built.

Start Decluttering Early

One of the most overwhelming parts of selling a home is realizing just how much you’ve accumulated over the years. The earlier you start decluttering, the less stressful the process will be when it’s time to move.

Start small. Tackle one closet or one room at a time. Create piles for items to keep, donate, or discard. Remember, letting go of physical items doesn’t mean letting go of the memories. It simply means making space for new ones in your next chapter.

If you find it difficult to part with certain sentimental items, consider designating a keepsake box for small mementos that carry deep meaning. This allows you to hold on to the most important pieces without feeling overwhelmed by clutter and allows the home to be ready for showings and positions the home to sell for top dollar.

Focus on the Future, Not Just the Past

While it is natural to feel nostalgic, it is also important to shift your focus toward the exciting opportunities ahead. Whether you are downsizing, upsizing, or relocating, think about what your next home will offer. Create a vision board or jot down a list of things you are looking forward to in your new space.

Focusing on the future will help balance the emotions of leaving your current home. Creating a simple reminder that while you are leaving one place behind, you are also entering into something new and exciting.

Lean on Your Real Estate Professional

Selling a home is a major life transition. You shouldn’t have to navigate it alone. Partnering with a trusted real estate agent can ease the burden significantly. Your agent will guide you through the listing, staging, and selling process while also offering valuable perspective and support.

Beyond logistics, your real estate agent can offer insights into market trends, pricing strategies, and negotiating tactics. Their guidance allows you to focus less on the technical details and more on preparing for your next chapter.

The sooner you get your agent involved, the smoother your home-selling process will be. With their market expertise, they’ll assess your home’s value, recommend improvements, and develop a personalized plan to help you achieve the best possible price.

Your agent may suggest professional staging, improving curb appeal, or small upgrades to boost your home’s marketability. Whether you move out or stay during the selling process, your agent will guide you every step of the way to ensure your home shows at its best.

Ready to get started? If you don’t have an agent yet, click here to get connected with one today.

Create a “Moving Game Plan”

The logistical side of moving can quickly become stressful without a plan. Minimize chaos by creating a clear, step-by-step game plan for your move. Start by setting target dates for decluttering, packing, and hiring professional movers, if needed.

Having a clear plan in place allows you to break the process into manageable pieces, reducing last-minute stress and ensuring a smoother transition to your new home.

Get an Inspection & Make a Game Plan for Key Repairs

Conducting a pre-inspection aids you in understanding your home’s condition and helps you prioritize repairs. Some major fixes like a new roof or water heater may be necessary while other cosmetic updates may not be required. Talking with your agent can help you decide what is most important based on current market conditions and buyer expectations and help you with your timeline. If your budget is tight, consider asking your agent about the Windermere Ready program.

Embrace the Journey

Finally, remember that selling your home is not just an ending—it is a beginning. Yes, you are leaving behind a place filled with memories, but you are also opening the door to new adventures, new neighbors, and new experiences.

Take time to appreciate the journey. Pause to reflect on how far you’ve come. Embrace the transition with gratitude.

Final Thoughts

While the process can be emotionally and physically challenging, taking intentional steps to declutter, plan, and lean on your real estate professional can significantly reduce your stress.

As you turn the page and step into your next chapter, remember that home is not defined by four walls, it is defined by the love, memories, and experiences you carry with you.

If you are ready to take the next step connect with us. We are here to help you navigate your journey.

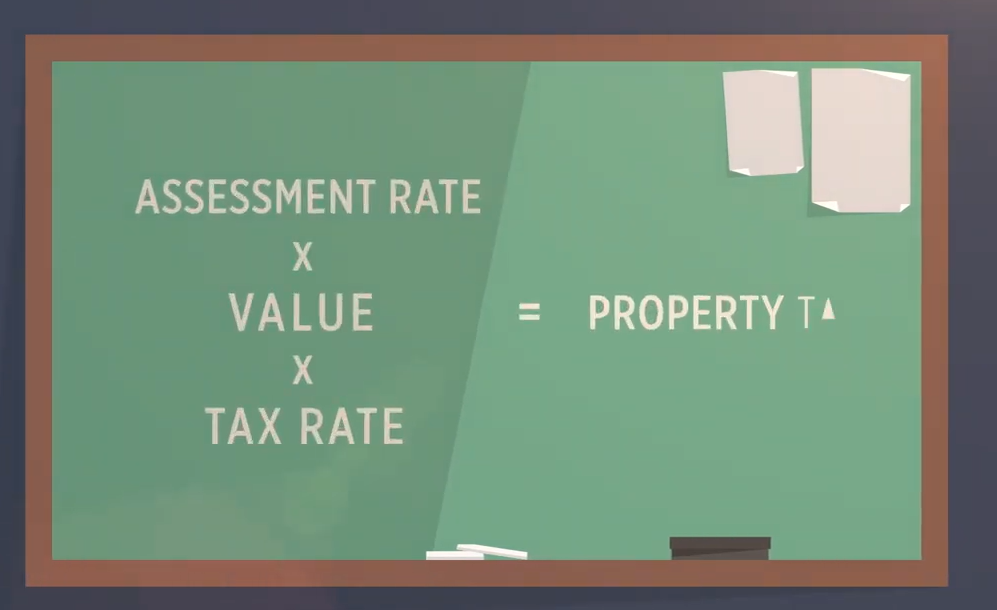

Understanding Property Assessments and Taxes in Island County

At Windermere Whidbey Island, we are committed to providing our clients with valuable insights and information about the real estate market on Whidbey Island, Washington. One topic that frequently comes up in discussions with our clients is how property assessments and taxes work in Island County. To help clarify this complex process, we recently had a presentation by Jason Joiner from People’s Bank, who previously served as the Deputy Assessor at Island County. His expertise has equipped us with the knowledge to better serve our clients, and we are excited to share these insights with you so that you can have an understanding of property assessments and taxes in Island County.

The Basics of Property Assessments and Taxes

In Washington State, property taxes are determined through a budget-based system rather than a rate-based system. Understanding this distinction is crucial for comprehending how property taxes are calculated in Island County. In a budget-based system, the county sets its annual budget, and property owners contribute a portion of that budget based on the assessed value of their property. This means that the total property tax collected is determined by the budget, not the property tax rate.

For a more detailed explanation, we recommend watching this YouTube video that breaks down the basics of property assessments and their connection to taxes.

Lid Lifts and Property Tax Increases

Washington State law restricts property tax increases to 1% per year. However, it is sometimes necessary to raise the baseline beyond this limit to keep up with rising costs and inflation. This process is known as a “lid lift,” which requires voter approval. Essentially, voters may be asked every few years to approve a lid lift to ensure the county can continue to meet its budgetary needs without falling behind due to inflation.

Property Tax Rates in Island County

One of the benefits of living in Island County is our relatively low property tax rates compared to other areas in the state. This advantage is significant for property owners and is an important consideration for those looking to move to the area.

The Assessment Process

Island County is divided into six appraisal areas. Each year, county assessors are required to physically inspect one of these areas. The remaining areas are adjusted based on a conservative market-based increase. This method, known as the “catch up method,” means that property owners will typically see a more noticeable increase in their property value during the year their area is physically inspected.

This approach ensures that property values remain accurate and reflect any significant changes in the market or the property itself. However, it also means that property owners should be prepared for potential fluctuations in their assessed value from year to year.

Preparing for Potential Property Tax Increases

When purchasing a property, it is essential to budget for potential property tax increases, especially if the purchase price is significantly higher than the current assessed value. A good rule of thumb is to budget about 1% of the purchase price for property taxes. This conservative estimate helps ensure that buyers are not caught off guard by a substantial tax increase after their purchase.

The Role of Permits in Property Assessments

The Island County Planning Department provides a list of permits to the assessor’s office, which uses this information to adjust assessed values as needed. For example, a permit for a hot water heater replacement might not affect the assessed value, but a permit for a new kitchen would likely lead to an upward adjustment.

It is important to note that assessors conducting physical inspections are not reporting unpermitted improvements to the planning department. This means that while unpermitted improvements may eventually be discovered and assessed, the assessors themselves do not report these findings.

Appealing Your Property Assessment

If you disagree with your property assessment, you have the right to appeal. When you receive your assessment notice in June, you have 30 days from the date on the letter to file an appeal with the Board of Equalization. The instructions for filing an appeal are provided on the back of the notice. This process allows property owners to present their case and potentially receive a revised assessment.

Understanding the Workload of Assessors

It is worth noting that private sector appraisers typically charge around $800 per appraisal, while the Island County Assessor’s office receives about $23 per assessment. Despite this significant difference in compensation, the public often expects the same level of service and accuracy from county assessors. This disparity highlights the challenges faced by public sector assessors in maintaining high standards of service with limited resources.

Final Thoughts

Understanding the intricacies of property assessments and taxes in Island County can be daunting, but it is an essential aspect of property ownership. By familiarizing yourself with the process, you can better navigate your financial responsibilities and make informed decisions about your property investments.

At Windermere Whidbey Island, we are dedicated to guiding and educating our clients on all aspects of property ownership. Whether you are considering buying a new home, appealing your property assessment, or simply want to learn more about how property taxes work, we are here to help. Please feel free to reach out with any questions or concerns you may have. Let’s work together to make your real estate journey as smooth and informed as possible.

Windermere Whidbey Island is here to assist you every step of the way. If you are not currently working with a realtor and would like to, connect with us here.

The Orchestra of Real Estate

Have you ever wondered who all is involved during a real estate transaction? If so, follow along as we discuss the orchestra of Real Estate. Keep reading as we share how Realtors coordinate the players in every transaction.

In the world of real estate, orchestrating a successful transaction is akin to conducting a symphony. Behind the scenes, an ensemble of professionals comes together, each playing a vital role in bringing the deal to fruition. At the helm of this operation is the realtor, the conductor, who ensures that every note is played in harmony. Let’s take a closer look at the diverse cast of characters involved in a real estate transaction and how the realtor orchestrates their collaboration to create a seamless experience for buyers and sellers alike.

Staging Professionals:

Staging professionals specialize in enhancing a property’s appeal by arranging furniture, decor, and accessories to showcase its potential. Their expertise creates an inviting atmosphere that resonates with buyers and helps them envision themselves living in the home.

Photographers:

Photographers capture the essence of a property through stunning visuals that attract potential buyers. Their images highlight the property’s best features and create a compelling first impression in marketing materials.

Sign Companies:

Signage is a critical component of marketing a property, both online and offline. Sign companies design and install signs that grab attention and direct interested buyers to the property, increasing visibility and exposure.

Marketing:

Marketers develop comprehensive strategies to promote properties through various channels, including digital advertising, social media, and print materials. Their efforts ensure that listings reach the widest possible audience and generate interest from potential buyers.

Transaction Coordinators:

Transaction coordinators serve as the backbone of the transaction, managing paperwork, deadlines, and communications between all parties involved. They keep the process on track and ensure that nothing falls through the cracks.

Lenders:

Lenders provide financing to buyers, enabling them to purchase properties. They evaluate borrowers’ financial qualifications, underwrite loans, and facilitate the transfer of funds at closing. To learn more about the importance of using a local lender click here.

Title & Escrow:

Title companies conduct thorough searches to verify property ownership and facilitate the transfer of title from seller to buyer. Escrow agents hold funds and documents in trust until all conditions of the sale are met, ensuring a secure and transparent transaction. To learn more about escrows role in your transaction click here.

Insurance:

Homeowners insurance protects buyers against damage or loss to their property, while mortgage insurance protects lenders in case of borrower default. Both types of insurance provide financial security and peace of mind to parties involved in the transaction.

City Officials:

City officials play a pivotal role in the real estate process by ensuring compliance with local regulations and zoning ordinances. They oversee permits, inspections, and other administrative tasks that are essential for a smooth transaction.

Contractors:

Contractors are the craftsmen who bring properties to life through renovations, repairs, and improvements. From painters to plumbers, their expertise is essential in preparing a property for sale or addressing any issues uncovered during inspections.

Lawyers:

Legal professionals provide invaluable guidance on matters such as contracts, disclosures, and property rights. They ensure that all legal aspects of the transaction are handled correctly and protect their clients’ interests throughout the process.

In the intricate dance of a real estate transaction, every player has a role to play, and every role is essential to the symphony’s success. Behind the scenes, the realtor orchestrates this collaboration, ensuring that each element comes together seamlessly to create a harmonious outcome for buyers and sellers alike. As the conductor of this ensemble, the realtor’s expertise and guidance are invaluable in navigating the complexities of the real estate market and guiding clients towards their goals. If you are considering buying or selling and are not currently working with a Realtor, connect with us here.

Utilize That Tax Refund to Benefit Your Future Self

While every tax refund is different, if you received a refund this year, it’s likely that it is larger than in years past. On April 15th CNET shared that:

“The average refund size is up by 4.6%, from $2,878 for 2023’s tax season through April 7, to $3,011 for this season through April 5.”

There is a good chance that your tax refund not only was larger, but it also may have hit your bank account by now. If you haven’t spent it already, keep reading for a couple ways you could leverage it with real estate.

First and foremost, purchasing real estate is like investing in yourself. Each payment you make towards your mortgage lowers your debt and increases your equity. Combine this increase of equity with the historical average home price increase of 5% per year, and it becomes clear that homeownership can be a powerful wealth-building strategy. Over time, not only do you build equity through mortgage payments, but your home also typically appreciates in value. Each payment further enhances your overall financial position. Can we agree that spending a little extra now on a mortgage of our own to pay out a greater return in the future could be worth it? If you are open to this idea of wealth building let’s discuss how you could utilize that tax refund to benefit your future self.

Saving for a Down Payment

One of the greatest obstacles for attaining home ownership is saving enough for a down payment. Your tax refund might just be the boost in income you needed to make homeownership a reality. Lucky for you the 20% down payment requirements of the past are long gone. However, there are benefits when you do put down 20% check them out here. Today, lenders have options as low as 3% down. If you are a military Veteran there are 0% down VA Loans. Learn more about them here. Check with your lender to see what you qualify for and if these loan types will benefit your home goals. If you are not currently working with a lender connect with us and we can help you locate a few.

Pay Closing Costs

Closing costs are the fees and expenses incurred when finalizing a real estate transaction. They typically range between 2% and 5% of the total purchase price of the home. These costs encompass various expenses, such as loan origination fees, appraisal fees, title insurance, and property taxes. Considering these expenses, directing your tax refund toward covering closing costs can help alleviate the financial burden at the time of closing.

Reduce Your Mortgage Rates by Purchasing Points

If rates today mean affordability is tight, consider talking to your lender about reducing your mortgage rates by purchasing points. You could use your tax refund to buy down your interest rate. Talk to your lender to see if you qualify and if this option is right for your homeownership goals.

Make Extra Payment Towards Your Mortgage and Reduce Overall Interest

Another alternative, if your loan allows for it, is to make additional payments towards your mortgage loan. Each additional payment reduces your total pay off amount. Your payment remains the same, it just means with each additional payment your mortgage will get paid off sooner. Check with your lender, but depending on your loan type, if you pay it off earlier your total interest paid is less than it would have been if you made regular payments.

Whether you are ready to buy now, or in the future, connecting with a trusted real estate professional that understands the process and your options to ensure that you are ready to buy is of the utmost importance. If you are not currently working with a Realtor, connect with us today. We can help you utilize that tax refund to benefit your future self.

Maximizing Your Purchasing Potential

When it comes to purchasing a home, understanding your buying power and strategically taking steps to enhance your position are key to maximizing your purchasing potential. Beyond just envisioning your dream home, it is crucial to recognize the numerical factors lenders consider when approving you for a mortgage. By strengthening the following key areas, you can elevate your financial standing and position and find success in a competitive housing market.

Strategies to Maximize Your Purchasing Potential

First and foremost, give yourself time to prepare. Change will not happen overnight. Be patient and give yourself grace. Create a list of attainable goals and make consistent efforts to reach them. Over time, you will see the difference. We suggest talking to a lender as soon as possible so they can help identify specific key areas unique to you. Overall, you can increase your buying power by preparing for a down payment, increasing your credit score, and reducing your debit-to-income ratio.

Prepare for a Down Payment

Before 1956, down payments needed to be 20% of the home’s sale price. In 1956, banks adjusted their regulations, permitting homebuyers to make down payments of less than 20%. There was a crucial condition attached to this change. Those who used this option would be required to make an extra monthly payment called private mortgage insurance (PMI). Essentially, PMI serves as a safeguard for the bank in case of default by the borrower. While 20% is not a requirement today, in fact, there are loan options as low as 0 down, there are significant advantages to putting 20% or more down.

Putting 20% down eliminates the requirement for the PMI fee, keeping more money in your pockets. Even more so, making a down payment of 20% or more distinguishes your offer. Doing so, makes it more attractive to sellers and potentially enables you to secure a reduced interest rate for your mortgage through negotiation.

Finally, the more money you put down upfront reduces your monthly mortgage payment and the overall amount of interest you will pay. This keeps even more money in your pocket.

Set aside funds each paycheck

Consider saving by earmarking a portion of each paycheck to bolster your down payment fund. You can steadily accumulate funds over time by setting a clear savings goal and allocating a consistent amount from each pay period. If you prefer a more structured approach, consider opening a separate savings account dedicated solely to your down payment savings. Sometimes, you yield higher interest rates with a savings account.

Explore alternative avenues to boost your income

If you have skills or interests beyond your primary job, consider seeking part-time or freelance opportunities to generate additional revenue. You can expedite your journey toward homeownership by channeling this extra income directly into your down payment fund.

Review your current spending habits

Commit to reducing excessive spending. Perhaps commit to one less meal out a week, make your coffee at home instead of from the coffee shop, or skip out on the big vacation this year to increase your down payment. Consider using one of the many money management apps like Rocket Money to help you with your spending and saving goals.

Increase Your Credit Score

Your credit score is a factor considered when applying for a mortgage. A higher credit score maximizes your purchasing potential by potentially reducing your interest rate. The lower your rate, the more purchasing power you have.

To boost your credit score, prioritize paying down outstanding balances on your credit cards. Prioritize those with high-interest rates. Avoid opening unnecessary new lines of credit and steer clear of significant purchases leading up to the period when you’re ready to make a home offer. Remember that student loans also affect your financial profile, so consistently making payments will enhance your overall credibility with lenders.

Reduce Your Debit-To-Income Ratio

Lenders not only look at your creditworthiness, but they also consider your debt-to-income ratio. How much money do you owe vs. how much you make. This is important because you must be able to afford the home you are buying, pay off your current debts, and have enough money for day-to-day living.

The front-end ratio

Lenders assess your ability to repay a mortgage by examining your housing ratio. This ratio represents the percentage of your monthly gross income that will be allocated to your mortgage payment. It is calculated by dividing your monthly mortgage payment by your monthly gross income. A higher ratio indicates a greater risk of default.

The back-end ratio

The back-end ratio plays a crucial role in assessing your financial health. It gauges the percentage of your monthly income allocated to debt repayment. Included in this calculation is mortgage payments, credit card bills, student loans, and other loan obligations. It is calculated by dividing your total monthly debt expenses by your gross monthly income. This ratio offers insight into your ability to manage debt responsibly and affects your loan eligibility.

Increasing your credit score, reducing credit card balances, and making regular, on-time payments toward your loans contribute to lowering your overall debt while enhancing your debt-to-income ratios. This positive financial behavior demonstrates your ability to manage debt responsibly. In turn, it strengthens your financial position and enhances your buying power.

These key factors are not the only aspects of purchasing a home but they play a significant role. We strongly suggest speaking to a trusted lender early on to get specific recommendations based on your unique financial situation. Remember, increasing your buying power is a lengthy process. Having a specific strategy is key to staying on track. Make an attainable plan so that when your dream home comes along, you are in the best financial position to make it your reality.

Connect with us to get the conversation started.

Spring Cleaning

Spring cleaning has long been a cherished tradition embraced by households worldwide. Stemming from a practical need to freshen up living spaces after the long winter months, this annual ritual has evolved into a symbol of renewal and rejuvenation. Beyond simply tidying up, spring cleaning holds significant importance for both physical and mental well-being. By clearing out clutter, dust, and grime accumulated over the winter, we create a cleaner and healthier environment for ourselves and our families. Moreover, the act of spring cleaning can have positive effects on our mindset, providing a sense of accomplishment, satisfaction, and a renewed energy to tackle new challenges. Embracing this tradition allows us to start the new season on a clean slate, fostering a sense of optimism and positivity as we welcome the warmer days ahead.

Follow along for a comprehensive spring cleaning checklist to help you tackle every corner of your home:

Declutter and Donate

- Make your home more inviting by decluttering. Go through each room and declutter by getting rid of items you no longer need or use.

- Donate, sell, or discard items that are no longer serving a purpose for you. Consign your items at places like My Sisters Closet, or host a yard sale and feel a sense of accomplishment when you can fund something new. Whatever you find yourself still left with donate to a local thrift store. Island Thrift, WAIF Thrift Shop , and Treasure Island-Antique and Thrift are just a few of the many options on Whidbey Island.

Dust

- Open your windows and breathe a breath of fresh air.

- Dust all surfaces, including shelves, countertops, furniture, and electronics.

- Don’t forget to dust ceiling fans, light fixtures, and vents.

Clean Windows

- Spring brings so much outside beauty. Make sure you can enjoy it all with sparkling windows.

- Wash windows inside and out, including the window frames and sills. If your window has weeping holes, be sure to make sure they are not clogged so that excess water can drain properly.

- If cleaning your windows is out of reach there are companies like A Clean Streak or Oh Say Can You See that can help.

- Clean blinds, curtains, or drapes according to manufacturer’s instructions.

Vacuum and Clean Floors

- Vacuum carpets and area rugs thoroughly.

- Sweep and mop hard floors, paying special attention to corners and baseboards.

Deep Clean Kitchen and Restrooms

- Clean and disinfect countertops, cabinets, and drawers, all bathroom surfaces, including sinks, toilets, and tubs/showers.

- Clean appliances inside and out, including the refrigerator, oven, microwave, and dishwasher.

- Degrease stove hood and filter.

- Scrub tile grout and remove any mold or mildew.

Organize Closets and Cabinets

- Out with the old and in with the new… or maybe just move the sweaters to the back (we are still in the PNW and occasionally will still need those sweaters), but break out the vibrant tank tops it is spring already!

- Declutter and organize closets and cabinets, donating or discarding items as needed.

- Use storage bins or baskets to keep items organized and easily accessible.

Freshen up Bedding

- Launder bedding, including sheets, pillowcases, and duvet covers.

- To increase the life of your mattress, rotate and flip it for even wear.

Clean Upholstery and Furniture

- Vacuum upholstery and cushions to remove dust and debris. Make sure you get behind and underneath.

- Spot clean stains and spills on furniture.

Tidy Outdoor Spaces

- Sweep or pressure wash outdoor patios, decks, and walkways.

- Clean outdoor furniture and cushions.

- Trim bushes, trees, and clean up garden beds.

Inspect and Maintain

- Ensure your families safety every season.

- Check smoke detectors and carbon monoxide detectors, replacing batteries as needed.

- Test and clean ceiling fans.

- Schedule routine maintenance for HVAC systems, plumbing, and electrical systems.

Final Touches

- Brings some of the outside in.

- Add finishing touches such as fresh flowers or plants to bring life into your space.

- Sit back, relax, and enjoy your freshly cleaned and organized home!

Spring cleaning isn’t just about tidying up—it’s also an essential part of home maintenance and preparation for the warmer months ahead. For homeowners, it’s an opportunity to refresh their living spaces and ensure that their property is in top condition. Beyond the aesthetic benefits, a thorough spring cleaning can enhance the value of a home by improving its curb appeal and overall appeal to potential buyers. By decluttering, organizing, and performing deep cleaning tasks, homeowners can showcase their property’s full potential and make a positive impression on prospective buyers. Additionally, addressing maintenance issues early can help prevent costly repairs down the line and contribute to the long-term health and durability of the home. So, as spring approaches, embrace the tradition of spring cleaning as a valuable investment in both your home and your well-being.

If you are considering selling this Spring, connect with us.

To help get you motivated listen to our Spring Cleaning Playlist Here.