Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Benefits of Putting 20% Down on a House

If you read our, “How Long Does it Take to Save For a Down Payment?” article back in October, you know you don’t need a 20% downpayment to purchase a home because there are many alternative options available to you. However, while there are a plethora of options that you might qualify for, let’s look deeper into how putting 20% down could benefit you overall. You can find tried and true suggestions for saving up your downpayment here if you don’t have 20% saved up already. Keep in mind you can connect with us at any time to get personalized suggestions for what would work best for you in your unique situation.

In this article we are going to discuss how putting 20% down can help you get a lower interest rate, pay less overall, stand out in this competitive market, and avoid paying for PMI. Let’s get started.

Lower your interest rate:

A 20% down payment vs. a 3-5% down payment demonstrates to your lender that you are financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate will likely be.

Pay less overall:

The larger your down payment, the smaller your loan amount will be for your mortgage. If you are able to pay 20% of the cost of your new home at the start of the transaction, you will only pay interest on the remaining 80% of the cost of the home. If you put down 3.5 %, the additional 16.5% will be added to your loan and will accrue interest over time. This will end up costing you significantly more over the lifetime of your home loan.

Stand out in this competitive market:

In a market where many buyers are competing for the same home, sellers often like to see offers come in with 20% or larger down payments. Many buyers were hoping for the typical winter “slow-down” where they could see a less competitive market but that has proven not to be the case this year. Read more in our article, “Thinking the Housing Market is Going to Slow down this Winter? Think Again!” The seller in this current scenario gains the same confidence as the lender. You are seen as a stronger buyer with financing that is more likely to be approved. Therefore, there is a significantly higher chance that the deal will go through with a 20% downpayment.

Avoid paying for PMI:

You might be asking yourself, what is PMI? Freddie Mac explains,

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. . . . Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment.”

As mentioned earlier, if you put down less than 20% when buying a home, your lender will see your loan as having more risk than those who do put 20% down. PMI helps lenders recover their investment in you in the case that you are unable to pay your loan. However, this insurance is not required if you are able to put down 20% or more. In turn, this saves you from paying those extra fees.

Oftentimes, sellers looking to move to a larger or more expensive home are able to take the equity they earn from the sale of their house to put 20% down on their next home. The equity homeowners have today, creates an advantageous opportunity to put those savings toward a larger down payment on a new home.

If you are considering buying or selling or just want to talk about this in more detail, connect with us. We are here to help.

Things to do Today to make you a Homeowner Tomorrow

As the gap between the cost of rent and the cost of a mortgage continues to close, we see an increasing number of renters interested in buying. But how can renters make the transition to owners?

The purpose of this article is to help renters implement three critical changes today to help them successfully purchase a home tomorrow. If implemented correctly, these changes will help renters overcome the feeling of never being able to purchase a home.

Start by talking with a local lender

Do your research. Find a trusted lender in the location you are planning to purchase your home. Why is it important to use a local lender? Each housing market is different depending on location. Despite the similarities in names, what might be happening in San Francisco may not be happening in San Antonio. It is important to talk to a lender that is not only familiar with but understands the current local market and can explain to you what it takes to become a first-time homeowner. Check out our full article here. Your trusted advisor can then look at your specific financial situation and make suggestions to help you navigate the local market, meet your specific needs, and discuss your available options. This conversation can help you build your timeline for when it is right for you to purchase. Having the right team of real estate and lending professionals on your side can help tremendously when planning for your first home. Together they can help you determine your goals, what you can afford, and help you get pre-approved when you are ready. Need help finding a lender? Click here.

Reduce your debt and build your credit

Your first step should be knowing your credit score and what it means. Check out this article here for more information on credit scores. According to the HUD, the average credit score of first-time homebuyers is 716. There are many online tools that can help you determine your credit score. If you don’t already know yours it would be advantageous for you to find out.

If you determine that your score is below 716, don’t freak out.

First, 716 is just an average which means that there are homeowners with credit scores both above and below that number. Knowing your score gives you a snapshot of how you are doing financially and helps you know how to adjust accordingly to reach your goals.

Second, there are numerous ways to increase your credit score BEFORE you apply for your home loan.

- HUD’s number one recommendation is to reduce your debt as much as possible. Start by reducing your current spending. This will not only help you have less debt, but it will also help you have more money to pay down your current debts. Start small, perhaps purchasing one less coffee a week or choosing water instead of the soda or martini. These small sacrifices now will add up to big wins later. We recommend TrueBill as an app that can help find hidden savings by canceling subscriptions you don’t use anymore or negotiating your existing subscriptions down. It can also help you develop and stick to a budget!

- Pay all your bills on time. Set up auto payments to avoid late payments.

- Use your credit card responsibly.

When you have your debt in a manageable place…

Start saving

It might already feel like you are barely making it. But it has been proven that setting aside even small amounts can make it possible for you to save for a down payment on a home over time. Having funds in savings is also taken into consideration when getting pre-approved for a home loan (See why getting pre-approved is imperative). You don’t always need a large down payment when buying a home but you will need a good house fund saved up for ongoing maintenance and repairs.

Many experts suggest using a hidden savings or a “sinking fund” when saving for your down payment. This is an “out of sight out of mind” savings account. Once money goes in you don’t take it back out till you are ready. Make sure you keep it separate from your emergency fund or your short-term savings for expenses. Set small attainable goals that make you feel accomplished rather than the large goal that might feel daunting and overwhelm you. Are you ready for the challenge?

See how long it takes the average person earning a medium-income in America to save for a down payment here.

In conclusion, get some professionals on your team by talking with a lender (ask your trusted Windermere Broker for recommendations) if you don't have an agent contact us here and we will get you connected, build credit, and start saving!

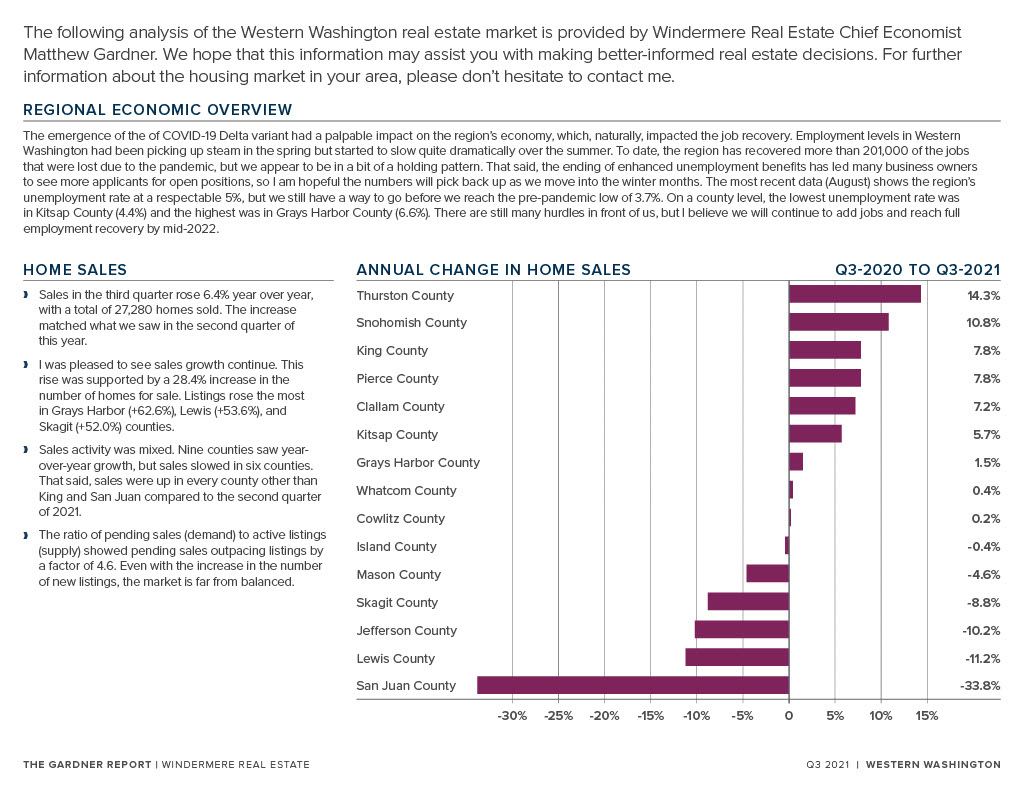

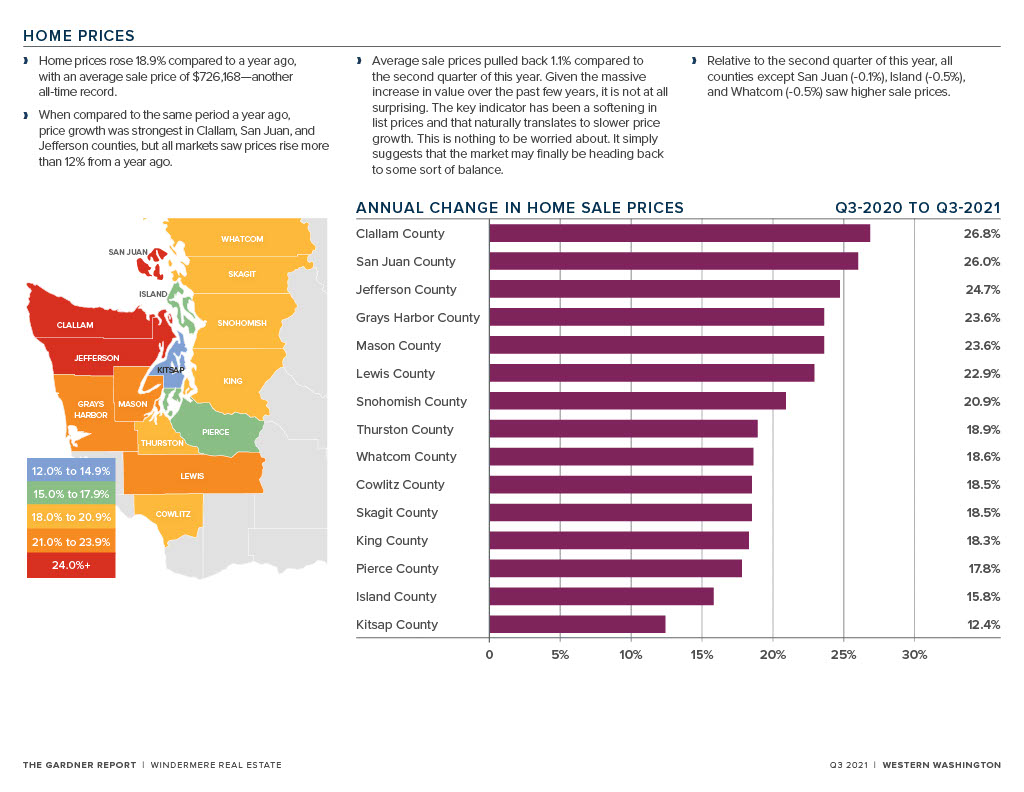

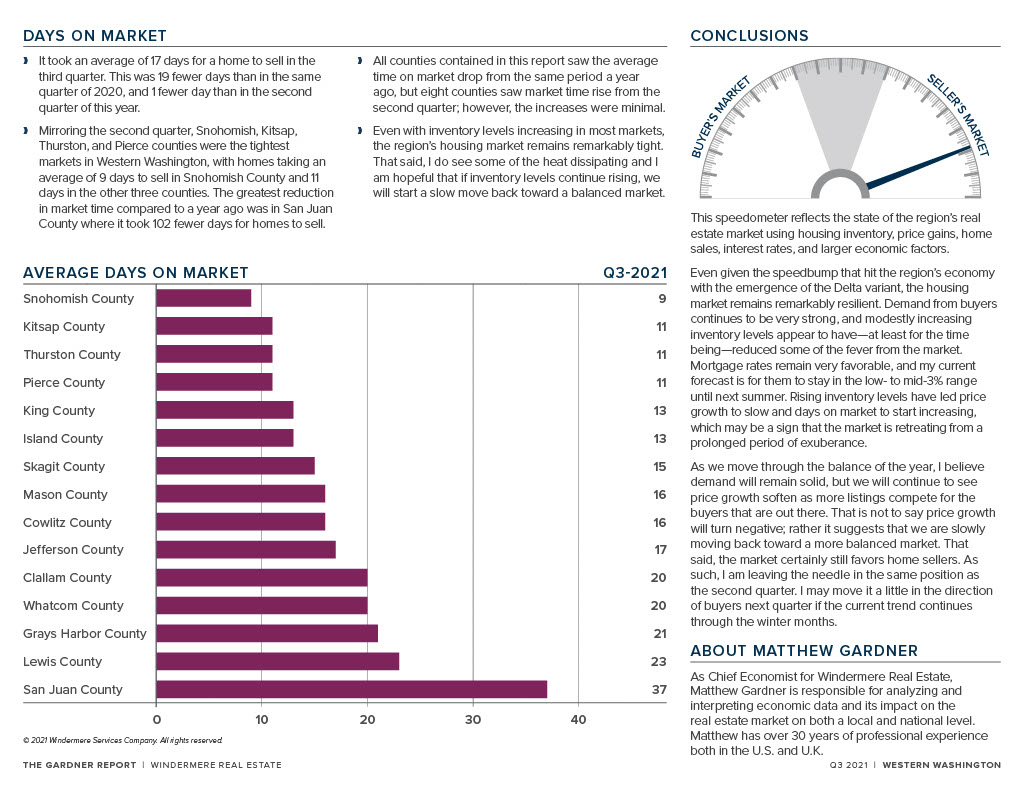

Q3, 2021 Gardner Report | Western Washington

Natures Halloween Decorations

Dun dun. Dun dun. Dun dun…. They’re here….. nature’s Halloween decoration…

It’s Spider Season!

It comes without fail every year. In what feels like a blink of an eye every tree, bush, and building corner is covered in shiny interwoven silk with a beady-eyed creature lurking somewhere nearby.

If you’re like most people, this is probably your least favorite time of the year. The occurrence of these little eight-legged animals provokes feelings ranging from mild disgust to outlandish fear. A lot of this fear comes from misinformation we’ve been given for a long time. So, let’s debunk some of these myths, shall we?

Myth #1 – “Spiders have dangerous venom that could kill.”

Although it is true all spiders have venom (yes, ALL spiders); only a VERY small number have the ability to harm humans, and of those, few are fatal. Even a bite from the most notorious arachnid, the Black Widow, is mostly non-life-threatening for healthy adults. Thanks to modern medicine our access to antivenom has increased dramatically.

Myth #2 – “We have Brown Recluses and Black Widows on Whidbey Island.”

No, you did not see a Brown Recluse in your bathtub and the black spider on the bush outside is not a Black Widow. Although these spiders do live in Washington State, the vast majority of them live on the east side of the Cascade Mountains. Sightings of these spiders in western Washington is very rare and practically unheard of for Whidbey Island.

So, what is the “scary” brown spider in your bathtub? We’re glad you asked! Here are 3 of the most common spiders to see on Whidbey:

-

The Common House Spider

Yes, there is a spider called the Common House Spider. Although there are several subspecies, they are all harmless but enjoy dry, warmer areas. You’ll often spot these spiders in the unused corners of your house hanging out and waiting for a fly to make its way towards them.

-

Wolf Spiders

This was probably the spider is the bathtub! Also called a Wood Spider, these little eight-legged friends are plentiful on the island and admittedly a little intimidating. To an untrained eye, these guys look a lot like a Brown Recluse; however, they are actually a little bigger and 100% harmless. You’ll find them mostly outside on the ground as they are not the best climbers and typically don’t build webs.

-

European Cross Spider

Probably the most majestic of our Whidbey Island spiders, you can thank these large rear-ended arachnids for the early Halloween decorations you find in your trees and bushes. Found almost exclusively outside, these beauties are the kings of web making. They are one of the few spider species that weave circular webs. Although mildly annoying, you can’t help but admire their workmanship.

So, there you have it. No need to take a torch to that tree this fall or scream when you see the tiny brown friend hiding in the corner. Just scoop them up and take them outside! Spiders are actually a great help when it comes to getting rid of actual pests like mosquitos or termites, and with any luck, they might just do the Halloween decorating for you this year.

4 Online Resources That will Blow Your Mind!

…and help when buying vacant land on Whidbey Island.

ICGeo

This is a sophisticated GIS mapping tool for Island County that can show layers and layers of geographically specific data overlaid on a map. Just turn on the layers of data you are interested in and search till your heart is content!

Island County Public Portal

Use this tool to look up a parcel number or a street address to determine if there are any site registrations, septic permits, or septic as-builts done for the parcel. It will also disclose any permits a property has recently applied for and its status.

Groundwater Spatial Analysis Report

This tool analyzes the potential groundwater quality at any given spot on the island by grabbing the data on wells within 1/8 mile of the point you choose on the map (or the nearest 40 wells). It automatically generates a phenomenal report. Just submit the application and the report is emailed to you almost immediately. This document will offer you more detailed information on what you get in the report

Washington Coastal Atlas Map

With the Shoreline Photo Viewer, you can compare what has happened to any stretch of shoreline over the last 50 years through photography! This tool uses 5 photo sessions capturing images of our shoreline all the way back to 1970. Even if you are not currently buying waterfront land this is a fun tool to compare what has happened to any section of our shoreline. There are even aerial photos from the 1940s. Check out the image below taken before Rolling Hills or Penn Cove Park were developed.

To find more amazing tools at your disposal or to get help using these tools to find specific information you can call us, and we will connect you with one of our knowledgeable Windermere brokers. You don’t have to be actively selling or buying a home! We just love to help! Contact us here.

Is the Oak Harbor Housing Market Getting Squishy?

Written by: Kristen Stavros

16 September 2021

There is a general feeling amongst brokers that the Oak Harbor market has softened up just a bit. As Branch Manager and Co-owner of Windermere Whidbey Island I pay close attention to what my brokers are seeing and feeling out there in the market. When I begin to sense a theme I go to the numbers to see if they are telling the same story.

I’ll be really curious to see how these numbers change when we can add September data to them but I’m seeing the teensiest sign that there may be some easing.

For the first time all year, we’ve seen a dip in closed sales in August.

At the same time, new listings continue to rise every month.

Average days on market has plateaued.

Does this mean buyers can start getting homes for less $$$?

The answer is emphatically, NO. As you can see from the graphs below prices continue to climb, inventory is still at a record low, and homes are still moving off the market incredibly fast. This just means that instead of being up against 10 other buyers you now may be up against just 2-3 other qualified buyers. Instead of great homes going for up to 10-20% over list price, the good ones may just end up 5-8% over list. The pressure on buyers is still decidedly strong but the dial has been turned down ever so slightly.

Average Price Per Square Foot.

Months’ Supply of Homes (based on closed sales).

Average Days on Market.

Sellers still have a fantastic advantage in this market but things are changing weekly so we are encouraging sellers to not get too greedy or assured because doing so may mean you overprice the market, lose the opportunity to garner multiple offers out of the gate, and ultimately make less profit on your home.

Working with a smart and sophisticated listing agent has never been more important in the previous 3 years than it is RIGHT NOW. You need someone who is really going to take their time analyzing the market against your specific home before giving you pricing advice. Call us today to be connected with a market pricing expert!

This analysis focuses just on the Oak Harbor market but we have the same analysis going on for all of Whidbey Island! If you are interested in knowing more about any aspect of Whidbey Island real estate let us know and we are happy to share.

Set Yourself up for Success by Doing These 7 Things When Buying Your First Home

Buying your first home can be easy when you are adequately prepared and you have a good agent on your side. But where to start and what actions are most important? We will get you pointed in the right direction. Let’s get started!

-

Know your credit score.

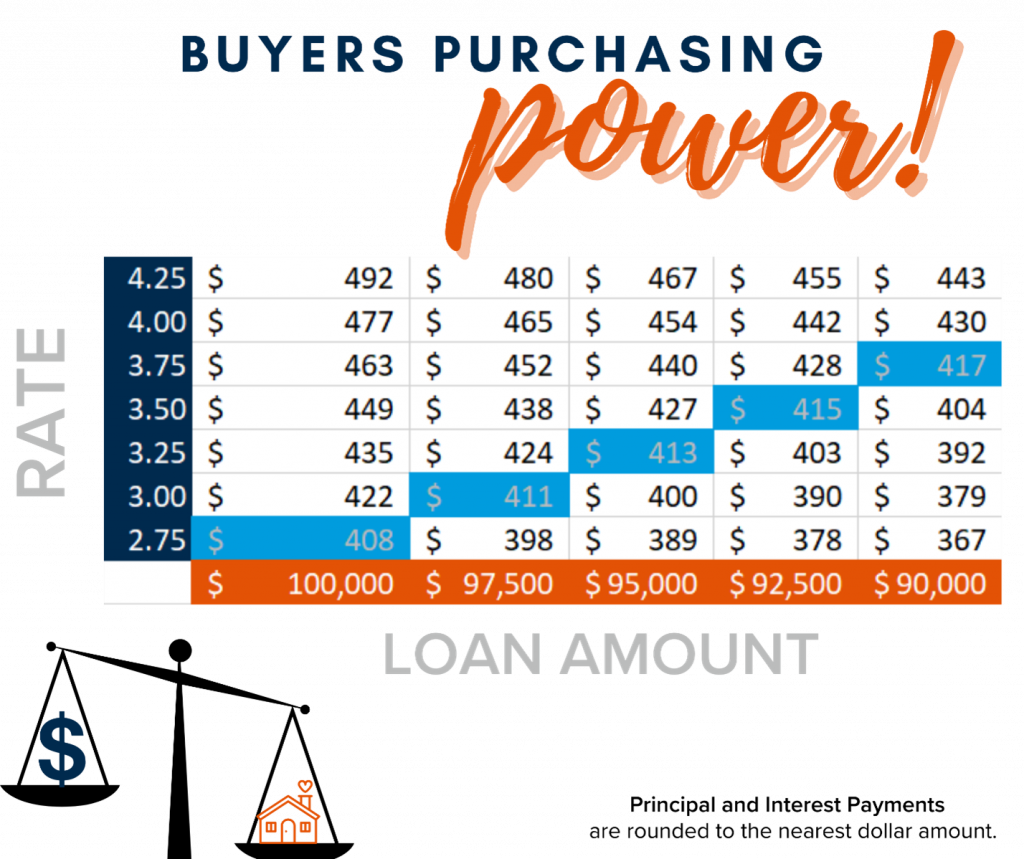

Many first-time homebuyers fail to recognize that one of the most important factors in getting approved for a mortgage is their credit score. The health of the score determines not only the interest rate but also whether they will be approved for a mortgage in the first place. Some people wonder why the interest rate really matters. The truth is that the slightest difference in rate can mean big money over 30 years! As the chart below demonstrates, a lower interest rate helps buyers afford a higher-priced house and still pay less monthly. Check out this article to learn more about Credit score rankings and what they mean.

-

Set a clear budget and stick with it.

Another big mistake first-time homebuyers make is not budgeting realistically and then finding out they cannot really afford the house they chose. A great way to get an idea of how much you should realistically spend on a mortgage is to determine your debt-to-income ratio. This number can be calculated by adding all your monthly debt payments (mortgage, credit card bill, car payment, etc.) together and then dividing by the gross monthly income. A conservative percentage of your income spent paying down debt would be 20-25%, a medium would be 25-30%, and a high would be 30-38% (or higher when using gross income vs. net).

-

Remember there are other fees other than the mortgage payment.

Homeownership comes with fees and other bills that you may not have as a renter. In addition to principal and interest on the mortgage payment, there will be real estate taxes and homeowner’s insurance. Check to see if the home is part of a homeowner’s association as there may be annual or monthly dues for that (a great agent will let you know about this). These fees typically show up as part of the mortgage payment. However, what is often forgotten or inaccurately calculated is the utility bills like water, sewage (or septic inspections/pumping), garbage, and energy bills. Furthermore, unlike renting if a pipe breaks or roof leaks there is no maintenance man that just shows up to repair it. Remember to budget for the maintenance of the home. This includes mowing the lawn… do you have a lawnmower yet?

-

Leave a cushion.

As discussed, buying a home has a lot of upfront costs. A bank account that seemingly had a plethora of cash can quickly be drained after the down payment, closing costs, moving expenses, and furnishing a new home. Having a healthy emergency fund is so critical as a homeowner.

Check out this helpful article by Dave Ramsey.

-

Once steps 1-3 are completed get pre-approved.

Don’t just meet with any lender, be sure to find a highly reputable local lender that the top listing brokers recommend (this will give you a competitive advantage). Not only does the pre-approval give buyers a realistic idea of how much they can borrow, but it can also be the defining factor of whether or not they get the home. Let us explain. A pre-approval speeds up the process and demonstrates the person is a serious buyer, not just a lookie-loo. When it comes down to multiple offer situations, as we see so frequently now, it is critical to have the most well-presented offer. Showing the seller that you are not only serious but that you have been pre-approved for the funds needed to buy with a lender they respect sends a strong message that you are the one the seller should choose! Check out our local lenders here.

-

Ask questions about your options!

Not everyone’s situation is the same. Similarly, loans are uniquely created to fit individual needs. Historically, it has been thought that buyers need to come to the table with at least a 25% down payment. Today that is just not true. While it is always good to have money for your mortgage down payment, there can be alternative options if you don’t. VA mortgages can be secured for 0% down and conventional mortgages for as little as 3%. Check out these different mortgage types meant to uniquely fit your life.

-

Hold off on any spending spree and do not take out a line of credit.

Remember that “debt-to-income ratio” mentioned above? Your mortgage approval is linked heavily to this number. This is not the time to go out and buy a new sportscar, purchases new appliances, and or upgrade your electronics. Borrowing money after getting pre-approved increases the debt-to-income ratio, and this will be re-checked just prior to the loan being approved. Applying for a new loan or credit card will also likely decrease your credit score. If either of these things happen prior to closing it could mean losing the mortgage and the interest rate you locked in. So, hold off on spending or even giving out your social security number to anyone!

We hope this helps point you in the right direction. We would love to be your guide as you prepare and navigate the path to homeownership! Call us today and we can connect you with an expert Buyers Broker! 360.675.5953.

If you enjoyed this you might also like:

5 Most Affordable Neighborhoods Near Oak Harbor & NAS Whidbey

The Importance of Shredding

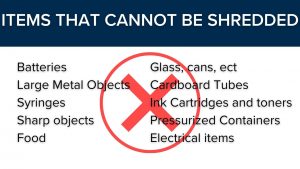

During or after the purchase or sale of a home you find a lot of paperwork that may have sensitive personal information. What do you do with all of that paperwork?! Throwing it in the trash could mean it falling in the wrong hands and used against you. The safest way to deal with old documents is to shred them. Below we go over what should and should not be shredded and why it’s important to protect your personal and sensitive information from falling into the wrong hands.

To help you, Windermere Real Estate/Whidbey Island is co-hosting a free Shred-it event on October 9th, 2021 and you are invited! Check out the details here!

Types of documents you should shred:

- Tax returns

- Photo IDs

- Bank Statements

- Voided Checks

- Employee Pay Stubs

- Credit Card information

- Copies of sale receipts

- Documents containing sensitive information such as names, addresses, phone numbers or emails

- Employee records

Top reasons you should shred:

- Prevent identity theft: In 2012, about 16.6 million U.S. residents over the age of 16 were victims of at least one identity theft incident according to the Bureau of Justice Statistics.

- Protecting your family, friends, and customers is the law: It is important that you take the extra steps to protect the people around you and shred sensitive information if you must write it down. Businesses that fail to abide by regulations protecting their customers’ personal and secure information are at risk of being fined for mishandling customers’ information.

- Protect your employees: Employees have a right to privacy and if you are throwing away documents you are not taking the necessary steps to protect their privacy or identity. Shredding is always the safest way to go.

- Space saved: by shredding all the unnecessary papers cluttering your office or your home you will create more room and less clutter ultimately you will feel more at ease and satisfied with your space.

If you’re wondering how long you need to keep ahold of different types of documents there are lots of different opinions but we liked the simplicity of this guidance https://www.suzeorman.com/resources/record-keeping

We are all in, for you! What that means is we believe that as realtors we can make a positive impact in our community and in the lives of the people around us. We do this not only by helping people purchase their homes but by staying active in our community and educating where needed. One thing we feel strongly about is protecting those people. Throughout the buying and selling process clients are guided through what kind of links are ok to accept, warned of scammers, and taught how to not fall prey to people trying to take advantage of them.

If you liked this blog you might also like:

What is your go-to for managing stress?

Preparing to List in the Whidbey Island Real Estate Market Right Now

Today’s housing market is full of exceptional opportunities for sellers. The large buyer demand combined with record-low housing inventory has created an optimal sellers’ market. This means that it can be a great time to sell your house if you are thinking about selling. However, one misconception is that sellers are guaranteed success no matter what. We are here to remind you, that is not always the case and to help set you up for the best possible success with some key points so you can avoid costly mistakes and win big when you make the move.

Price Your Property Right

It is a common misconception to think buyers will pay whatever we ask. This can be hard to imagine when the inventory is low like it is and we see homes sell well over listing price time and time again. However, even in a sellers’ market, it is of the utmost importance to list your house for the right price. Why? Because it will maximize the number of buyers that see your house. Listing above market value means that true target buyers may not ever see your property because it is listed out of their price range. Listing in the market value creates the best environment for bidding wars, which in turn is more likely to increase the final sale price meaning more money in your pocket. In fact, as of this writing, there are 10 homes just in North Whidbey that have been on the market for 11- 41 days which is a strong indication of being overpriced. This is only one of several examples of why it is important to price your property right the first time. To receive an in-depth look at the dangers of pricing above market value sign up here. A real estate professional is the best person to help you set the best price for your house so you can achieve your financial goals. Click here to get connected.

Keep Emotions in Check

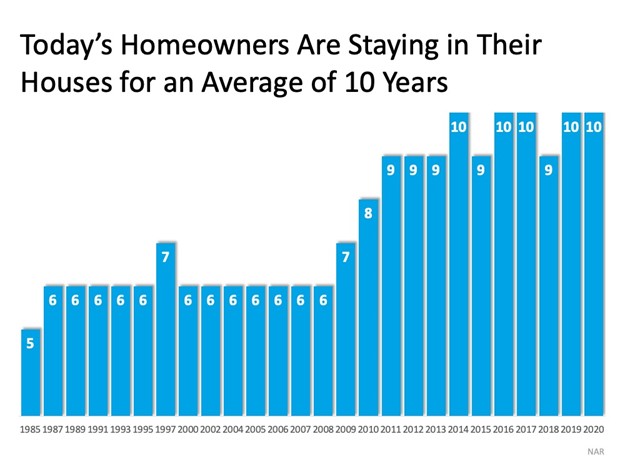

Today, homeowners are living in their homes longer than they have in the past. Looking at the chart below you can see that the average time a homeowner owned their home has doubled from 5 years in 1985 to 10 years now.

It only makes sense that as time in a home increases the emotional attachment to the home also grows. If it is the first home you purchased or it is the house where your children grew up, it is possible that it is extra special to you. Every room has memories. It is difficult to separate rational decision-making from that sentimental value and can take time to process.

For some homeowners, that connection makes it harder to differentiate the emotional value of the house from the fair market price. It is important to have a non-bias real estate professional help you along with setting the listing price and through the negotiations. We are here to help you.

Stage Properly

When we walk into our friends’ homes, we are often greeted by their children’s trophies, their accomplishments, newest toys, and probably a pile of mail on the counter they did not quite get to before we arrived. For the most part, we are all quite proud of our home décor and the things we have done to customize our homes to be fitting for our lifestyles and want to show it off. However, not all buyers feel the same way about your design and personal touches as you do. It is in your best interest to present your home in a way that a buyer can imagine themselves living there. That is why it is so important to make sure you stage your home with the potential buyer in mind.

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. Stage, clean, and declutter so they can visualize their own dreams as they walk through each room. A real estate professional can help you to get your home ready, stage it, and sell for top dollar.

At the End of the Day

Today’s sellers’ market might be your best chance to make your move. If you are considering selling your home, let’s connect today so you have the expert guidance you need to navigate through the process and prioritize these key elements.

Searching to learn more about Whidbey Island? You can continue exploring our community blog here!

Where Have All the Houses Gone?

In today’s housing market, it seems harder than ever to find a home to buy. Before the health crisis hit us a year ago, there was already a shortage of homes for sale. When many homeowners delayed their plans to sell at the same time that more buyers aimed to take advantage of record-low mortgage rates and purchase a home, housing inventory dropped even further. Experts consider this to be the biggest challenge facing an otherwise hot market while buyers continue to compete for homes. As Danielle Hale, Chief Economist at realtor.com, explains:

“With buyers active in the market and seller participation lagging, homes are selling quickly and the total number available for sale at any point in time continues to drop lower. In January as a whole, the number of for-sale homes dropped below 600,000.”

You can take a closer look at how the market here on Whidbey has progressed by clicking here.

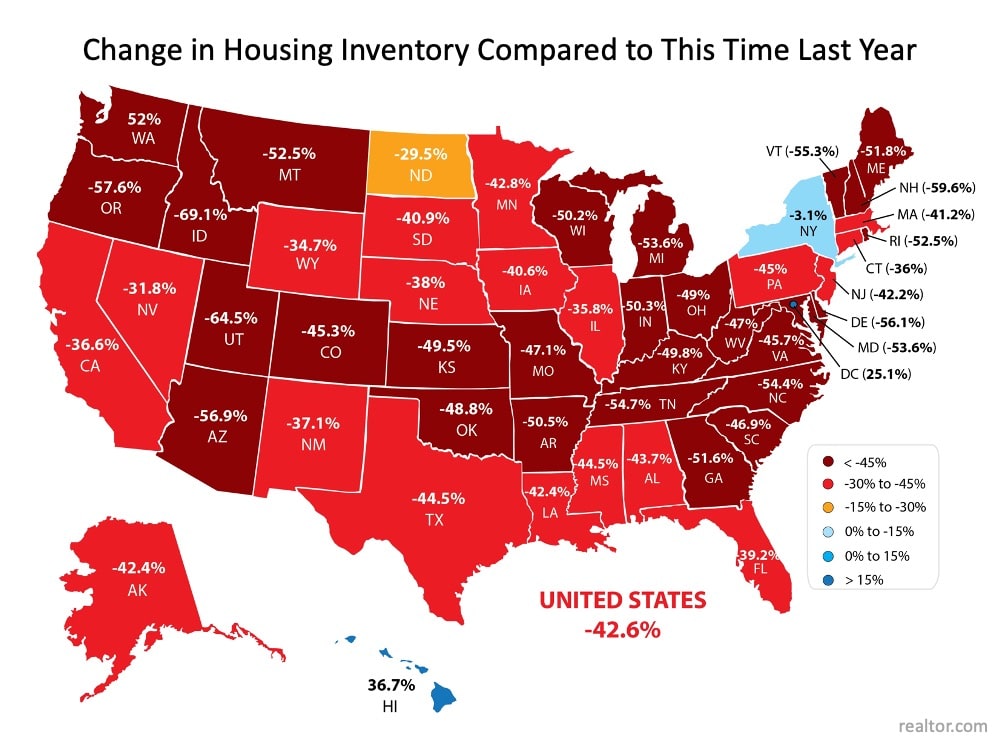

Every month, realtor.com releases new data showing the year-over-year change in inventory of existing homes for sale. As you can see in the map below, nationwide, inventory is 42.6% lower than it was at this time last year:

Does this mean houses aren’t being put on the market for sale?

Not exactly. While there are fewer existing homes being listed right now, many homes are simply selling faster than they’re being counted as current inventory. The market is that competitive! It’s like when everyone was trying to find toilet paper to buy last spring and it was flying off the shelves faster than it could be stocked in the stores. That’s what’s happening in the housing market: homes are being listed for sale, but not at a rate that can keep up with heavy demand from competitive buyers.

In the same realtor.com report, Hale explains:

“Time on the market was 10 days faster than last year meaning that buyers still have to make decisions quickly in order to be successful. Today’s buyers have many tools to help them do that, including the ability to be notified as soon as homes meeting their search criteria hit the market. By tailoring search and notifications to the homes that are a solid match, buyers can act quickly and compete successfully in this faster-paced housing market.”

The Good News for Homeowners

The health crisis has been a major reason why potential sellers have held off this long, but as vaccines become more widely available, homeowners will start making their moves. Ali Wolf, Chief Economist at Zonda, confirms:

“Some people will feel comfortable listing their home during the first half of 2021. Others will want to wait until the vaccines are widely distributed.”

With more homeowners getting ready to sell later this year, putting your house on the market sooner rather than later is the best way to make sure your listing shines brighter than the rest.

When you’re ready to sell your house, you’ll likely want it to sell as quickly as possible, for the best price, and with little to no hassle. If you’re looking for these selling conditions, you’ll find them in today’s market. When demand is high and inventory is low, sellers have the ability to create optimal terms and timelines for the sale, making now an exceptional time to move.

Bottom Line

Today’s housing market is a big win for sellers, but these conditions won’t last forever. If you’re in a position to sell your house now, you may not want to wait for your neighbors to do the same. Let’s connect to discuss how to sell your house safely so you’re able to benefit from today’s high demand and low inventory.

Continue to follow our local market with Windermere’s Cheif Economist, Matthew Gardner by clicking here.